For almost two years now I've stated that the U.S. is in a depression. I've been clear that I don't believe we are in a depression that is as big as the Great Depression was (though have never discounted the possibility). I've taken issue with the term "Great Recession" because it ignores history and tries to spin our actual economic situation. The term depression has not been used since the Great Depression, but was a common term before it. My point is that the evidence is clear we aren't in a garden variety recession, its a depression - but its not the end of the world. It seems that most economists and talking heads believe the term depression can only be used if you are talking about the end of society (ok, perhaps now I'm engaging in a bit of hyperbole, but not much).

Over at the Naked Capitalist blog (www.nakedcapitalist.com) Yves Smith has linked to a Washington Post blog which attempts to compare today's economy to that of the Great Depression. The comparison will likely change your mind as to how this economic environment should be termed, at the very least we should refer to it as a "Depression". Maybe "Silent Depression" should be the moniker.

Hit the topic above for the jump. I've also embedded two of the referenced videos.

Scott Dauenhauer, CFP, MSFP, AIF

Wednesday, December 29, 2010

Monday, December 27, 2010

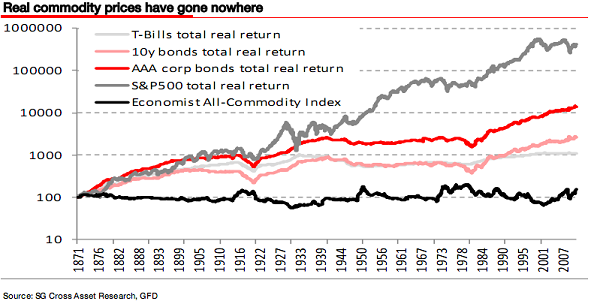

PragCap: COMMODITIES & THE 130+ YEAR BEAR MARKET

The Pragmatic Capitalist (www.pragcap.com) is one of my favorite blogs - even if we don't always agree. Mr. Roche has posted an excellent piece on Commodities which pretty much represents my thinking on the topic (perhaps ex-oil). I encourage you to read the entire piece, it is well worth it and provides an entirely different perspective than Glenn Beck's advertisers.

A few of my favorite portions:

Benjamin Graham Quote:

“An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.” - Benjamin Graham

Seth Klarman Quote:

“Buying anything that is a collectible, has no cash flow, and is based only on a future sale to a greater fool, if you will—even if that purchaser is not a fool—is speculating. The “investment” might work—owing to a limited supply of Monets, for example—but a commodity doesn’t have the same characteristics as a security, characteristics that allow for analysis. Other than a recent sale or appreciation due to inflation, analyzing the current or future worth of a commodity is nearly impossible.

The line I draw in the sand is that if an asset has cash flow or the likelihood of cash flow in the near term and is not purely dependent on what a future buyer might pay, then it’s an investment. If an asset’s value is totally dependent on the amount a future buyer might pay, then its purchase is speculation. The hardest commodity-like asset to categorize is land, an asset that is valuable to a future buyer because it will deliver cash flow, not because it will be sold to a future speculator.”

From Roche and Klarman:

There’s an interesting counterargument that can be made for a commodity such as gold, however. Doesn’t its currency like characteristics make it unique? Seth Klarman says no:

“Gold is unique because it has the age-old aspect of being viewed as a store of value. Nevertheless, it’s still a commodity and has no tangible value, and so I would say that gold is a speculation. But because of my fear about the potential debasing of paper money and about paper money not being a store of value, I want some exposure to gold.”

Hope you enjoy - you will also find the comment section provides even more learning opportunities.

Scott Dauenhauer CFP, MSFP, AIF

Wednesday, December 15, 2010

MISH: Chanos on China Bubble

China seems to be all anyone can talk about these days, is its centrally planned economy the wave of the future as some would like you to believe? My answer is no, the Soviet Union demonstrated that while a centrally planned economy can survive for a long time, it will never allocate resources correctly. Jim Chanos appeared on CNBC with a stunning outlook on China.

Humor Break: Colbert vs. Goldman Sachs

| The Colbert Report | Mon - Thurs 11:30pm / 10:30c | |||

| Goldman Sachs Lawyers Want Buckley T. Ratchford's Card Back | ||||

| ||||

Monday, December 06, 2010

Big Ben Explains Things

A few things that concern me:

Bernanke says that QE is not inflationary, but that he is worried about deflation and won't let it happen....if QE is not inflationary then how can it fight deflation?

I don't believe QE is inflationary, its an asset swap (as Bernanke states). This doesn't mean that others won't believe it is inflationary and push up asset prices as a speculation.

I think the worst quote is when the interviewer asks whether he is able to control things and he said he was "100% confident". Famous last words.

He says the goal is to lower rates, yet doesn't talk about liquidity traps or that QE has not worked in Japan.

Scott Dauenhauer CFP, MSFP, AIF

Bernanke says that QE is not inflationary, but that he is worried about deflation and won't let it happen....if QE is not inflationary then how can it fight deflation?

I don't believe QE is inflationary, its an asset swap (as Bernanke states). This doesn't mean that others won't believe it is inflationary and push up asset prices as a speculation.

I think the worst quote is when the interviewer asks whether he is able to control things and he said he was "100% confident". Famous last words.

He says the goal is to lower rates, yet doesn't talk about liquidity traps or that QE has not worked in Japan.

Scott Dauenhauer CFP, MSFP, AIF

The Q Ratio and Other Measures Showing Market Overvaluation

As the markets have raced up this year (close to 20%) I have remained sanguine and continue to believe that the stock market is overvalued. What are the measures that I use to make this determination? The linked to blog above updates a few measures that have proved valuable in determining the long-term return of the markets (in the short-term is has zero predictability). The three measures are:

The relationship of the S&P Composite to a regression trendline

The cyclical P/E ratio using the trailing 10-year earnings as the divisor

The Q Ratio — the total price of the market divided by its replacement cost

All three measures show significant overvaluation in the S & P 500, the Q ratio showing the worst at 49%. The charts are below:

The relationship of the S&P Composite to a regression trendline

The cyclical P/E ratio using the trailing 10-year earnings as the divisor

The Q Ratio — the total price of the market divided by its replacement cost

All three measures show significant overvaluation in the S & P 500, the Q ratio showing the worst at 49%. The charts are below:

Tuesday, November 16, 2010

PG: NY Fed Pres "We Are Not Printing Money"

A brief writeup over at the Pragmatic Capitalist regarding the misunderstanding of Quantitative Easing and the distortion it is causing. The Fed President is correct - the Federal Reserve is not "printing money" and the quicker we help people understand this (note I am not saying the quicker we support the Fed....I don't) the better off we will be.

Scott Dauenhauer CFP, MSFP, AIF

Scott Dauenhauer CFP, MSFP, AIF

Tuesday, November 09, 2010

PragCap: Understanding The Mechanics of a QE Transaction

Want to have your mind blown? The link above demonstrates how the Federal Reserve implements its policy of Quantitative Easing - it is not what those on TV lead you to believe (this is not a defense of Bernanke.....please don't misunderstand).

Here is an excerpt:

Scott Dauenhauer, CFP, MSFP, AIF

Here is an excerpt:

Before we begin, it’s important that investors understand exactly what “cash” is. “Cash” is simply a very liquid liability of the U.S. government. You can call it “cash”, Federal Reserve notes, whatever. But it is a liability of the U.S. government. Just like a 13 week treasury bill. What is the major distinction between “cash” and bills? Just the duration and amount of interest the two pay. Think of one like a checking account and the other like a savings account.

This is a crucial point that I think a lot of us are having trouble wrapping our heads around. In school we are taught that “cash” is its own unique asset class. But that’s not really true. “Cash” as it sits in your bank account is really just a very very liquid government liability. What is the difference between your checking and savings account? Do you classify them both as “cash”? Do you consider your savings accounts a slightly less liquid interest bearing form of the same thing a checking account is?

What is a treasury note account? It is a savings account with the government. So now you have to ask yourself why you think cash is so much different than a treasury note? What is the difference between your ETrade cash earning 0.1% and that t note earning 0.2%? NOTHING except the interest rate and the duration. You can’t use your 13 week bill to pay your taxes tomorrow, but that doesn’t mean it isn’t a slightly less liquid form of the exact same thing that we all refer to as “cash”. They are both govt liabilities and assets of yours.

When you own a t note you really just traded your “cash” for a slightly less liquid form of the same exact thing. If the Fed buys those t notes from you they give you back your cash minus the interest rate. That’s all there is to it. No change in the money supply. No change in anything except the rate of interest you were earning. If the government removes t notes then all they’re doing is altering the term structure of their liabilities. They’re not changing the AMOUNT of liabilities.

Scott Dauenhauer, CFP, MSFP, AIF

Stiglitz: Justice for Some

Some food for thought, hit the link above.

Scott Dauenhauer, CFP, MSFP, AIF

Scott Dauenhauer, CFP, MSFP, AIF

Friday, November 05, 2010

American is Not Greece: Why Glenn Beck and Most Economists/Politicians Are Wrong

"America is Greece" is the refrain you continue to hear from many politicians (particularly Republican). When searched on Google it comes up over 11,000 times. You also hear from the likes of Glenn Beck that if China stops buying our Treasury Bonds that in literally a few weeks the entire nation will collapse (kind of defeats the point of China's military....and ours I guess).

Is this hyperbole based on reality? Well, the answer is no, but there is some common sense that drives such rhetoric.

Before I go forward, let me just say that the more I learn about economics the less I feel I know. Having said that, I do know a few things.

First - the main point of Beck, Republicans and whomever is that America is spending too much - in this respect I think I can agree. I can also agree that, like Greece, we are likely to see riots in the streets if certain pension and health care benefits are cut. However, what Beck and others don't seem to understand is that the United States Government is nothing like Greece and WE DON'T NEED Chinese money to survive. In fact, interest rates don't HAVE to rise if the Chinese decide to get rid of their treasury bills.

The reality is that Greece is more akin to California than America. California cannot print its way out of budget problems because California can't issue its own currency. Greece doesn't issue its own currency anymore (they are on the EURO) and thus they can't print (read: devalue) their way out of there problems. The United States Government DOES NOT HAVE THIS PROBLEM. The U.S. can print as much money as it wants to pay off its debts. This means that it cannot outright default (they can, they just don't have too). If China stops buying our bonds, someone else will at either a higher interest rate or the Federal Reserve will buy them (please understand that this is not an endorsement of such policy, just the reality).

This doesn't mean that the actions of the Federal Reserve to deal with the very same issues that Greece has won't eventually harm us, I can assure it will. My point is that the America IS different because we have a different monetary regime.

Our current Federal Reserve leaders are leading us down the path of destruction, though they are of course being led by our politicians (don't be fooled by the last two elections - it really doesn't matter if its a Republican or a Democrat - neither can bring any kind of fiscal sanity about, nor do they want to....save just a few).

The Federal Reserve has embarked upon another round of Quantitative Easing - or printing money to buy assets. I do want to make it clear that while it appears the intention is to create inflation, I'm not positive it will. While it is true that the Fed literally pays for the Treasury Bonds with money that is created out of thin air, it is also true that this money doesn't actually stay in the system. If the Fed buys a Treasury bond and spends $1 billion the Treasury Bonds come onto the balance sheet of the Fed and stay there, the money goes to the people who sold the bond. The net change is that the Fed has $1 billion in bonds (of which interest is flowing to the Fed and is actually taken out of the system) and the entity who had the bond now has cash. There isn't any additional net assets in the system, the entity who had the bond now has cash (which could be used to buy more treasuries or other assets).

This is different than if the Federal Reserve called up the Mint and asked for $1 billion to be printed and then simply GAVE it to someone without receiving something in return. That would be pure money printing as the amount of cash actually in the system increased - that is potentially inflationary, but it isn't happening.

If you really want to research and understand our monetary system I suggest Austrian theory, reading Mike Shedlock and heading over to the Pragmatic Capitalist (he has some mind blowing stuff). I admit that my little explanation above likely places me in the category of Tim Allen's character on Home Improvement after trying to explain what his neighbor Wilson told him - but at least I'm willing to admit it.

Your Tim Allen Economist,

Scott Dauenhauer, CFP, MSFP, AIF

Is this hyperbole based on reality? Well, the answer is no, but there is some common sense that drives such rhetoric.

Before I go forward, let me just say that the more I learn about economics the less I feel I know. Having said that, I do know a few things.

First - the main point of Beck, Republicans and whomever is that America is spending too much - in this respect I think I can agree. I can also agree that, like Greece, we are likely to see riots in the streets if certain pension and health care benefits are cut. However, what Beck and others don't seem to understand is that the United States Government is nothing like Greece and WE DON'T NEED Chinese money to survive. In fact, interest rates don't HAVE to rise if the Chinese decide to get rid of their treasury bills.

The reality is that Greece is more akin to California than America. California cannot print its way out of budget problems because California can't issue its own currency. Greece doesn't issue its own currency anymore (they are on the EURO) and thus they can't print (read: devalue) their way out of there problems. The United States Government DOES NOT HAVE THIS PROBLEM. The U.S. can print as much money as it wants to pay off its debts. This means that it cannot outright default (they can, they just don't have too). If China stops buying our bonds, someone else will at either a higher interest rate or the Federal Reserve will buy them (please understand that this is not an endorsement of such policy, just the reality).

This doesn't mean that the actions of the Federal Reserve to deal with the very same issues that Greece has won't eventually harm us, I can assure it will. My point is that the America IS different because we have a different monetary regime.

Our current Federal Reserve leaders are leading us down the path of destruction, though they are of course being led by our politicians (don't be fooled by the last two elections - it really doesn't matter if its a Republican or a Democrat - neither can bring any kind of fiscal sanity about, nor do they want to....save just a few).

The Federal Reserve has embarked upon another round of Quantitative Easing - or printing money to buy assets. I do want to make it clear that while it appears the intention is to create inflation, I'm not positive it will. While it is true that the Fed literally pays for the Treasury Bonds with money that is created out of thin air, it is also true that this money doesn't actually stay in the system. If the Fed buys a Treasury bond and spends $1 billion the Treasury Bonds come onto the balance sheet of the Fed and stay there, the money goes to the people who sold the bond. The net change is that the Fed has $1 billion in bonds (of which interest is flowing to the Fed and is actually taken out of the system) and the entity who had the bond now has cash. There isn't any additional net assets in the system, the entity who had the bond now has cash (which could be used to buy more treasuries or other assets).

This is different than if the Federal Reserve called up the Mint and asked for $1 billion to be printed and then simply GAVE it to someone without receiving something in return. That would be pure money printing as the amount of cash actually in the system increased - that is potentially inflationary, but it isn't happening.

If you really want to research and understand our monetary system I suggest Austrian theory, reading Mike Shedlock and heading over to the Pragmatic Capitalist (he has some mind blowing stuff). I admit that my little explanation above likely places me in the category of Tim Allen's character on Home Improvement after trying to explain what his neighbor Wilson told him - but at least I'm willing to admit it.

Your Tim Allen Economist,

Scott Dauenhauer, CFP, MSFP, AIF

Wednesday, November 03, 2010

Humor Break: Is Obama A Keynesian? Rally For Sanity, 10/30/10

This is so funny, especially the one lady who just gets outraged!!

For the record - a Keynesian is a reference to an economic policy put forth by John Maynard Keynes (Government spending during down cycles), not someone from Kenya!!

Scott

For the record - a Keynesian is a reference to an economic policy put forth by John Maynard Keynes (Government spending during down cycles), not someone from Kenya!!

Scott

Monday, November 01, 2010

Taleb: Ten Principles For A Black Swan Proof World

I thought I'd start November out with some words of wisdom from Nassim Nicholas Taleb, author of two of my favorite books (Fooled By Randomness and Black Swan).

My favorite story that Taleb tells (which is appropriate for November) is that of the Thanksgiving Turkey.

——

CHARLIE ROSE: And what is the story of the turkey?

NASSIM NICHOLAS TALEB: In the book, I have the story of a turkey that is fed for 1,000 days by a butcher, and every day confirms to the turkey and the turkey’s economics department and the turkey’s risk management department and the turkey’s analytical department that the butcher loves turkeys, and every day brings more confidence to the statement. So it’s fed for 1,000 days…

CHARLIE ROSE: Gets fatter and fatter and fatter.

NASSIM NICHOLAS TALEB: Fatter and fatter. On the day when its comfort will be at its maximum, there is going to be a surprise. There will be a surprise for the turkey.

CHARLIE ROSE: Yes.

NASSIM NICHOLAS TALEB: There will be a surprise for the turkey’s economics department, all those Ph.D.’s. Will it be — after all, there’s maximum (inaudible)…

CHARLIE ROSE: But it’s not a surprise for the butcher, is it?

NASSIM NICHOLAS TALEB: Not a surprise for Charlie Rose as well. Not a surprise for humans. It’s a surprise for the turkey. So the whole idea here is we are not to be a turkey.

——

Who or what might be the next turkey?

And Now Taleb's Ten Principles:

1. What is fragile should break early while it is still small. Nothing should ever become too big to fail. Evolution in economic life helps those with the maximum amount of hidden risks – and hence the most fragile – become the biggest.

2. No socialisation of losses and privatisation of gains. Whatever may need to be bailed out should be nationalised; whatever does not need a bail-out should be free, small and risk- bearing. We have managed to combine the worst of capitalism and socialism. In France in the 1980s, the socialists took over the banks. In the US in the 2000s, the banks took over the government. This is surreal.

3. People who were driving a school bus blindfolded (and crashed it) should never be given a new bus. The economics establishment (universities, regulators, central bankers, government officials, various organisations staffed with economists) lost its legitimacy with the failure of the system. It is irresponsible and foolish to put our trust in the ability of such experts to get us out of this mess. Instead, find the smart people whose hands are clean.

4. Do not let someone making an “incentive” bonus manage a nuclear plant – or your financial risks. Odds are he would cut every corner on safety to show “profits” while claiming to be “conservative”. Bonuses do not accommodate the hidden risks of blow-ups. It is the asymmetry of the bonus system that got us here. No incentives without disincentives: capitalism is about rewards and punishments, not just rewards.

5. Counter-balance complexity with simplicity. Complexity from globalisation and highly networked economic life needs to be countered by simplicity in financial products. The complex economy is already a form of leverage: the leverage of efficiency. Such systems survive thanks to slack and redundancy; adding debt produces wild and dangerous gyrations and leaves no room for error. Capitalism cannot avoid fads and bubbles: equity bubbles (as in 2000) have proved to be mild; debt bubbles are vicious.

6. Do not give children sticks of dynamite, even if they come with a warning . Complex derivatives need to be banned because nobody understands them and few are rational enough to know it. Citizens must be protected from themselves, from bankers selling them “hedging” products, and from gullible regulators who listen to economic theorists.

7. Only Ponzi schemes should depend on confidence. Governments should never need to “restore confidence”. Cascading rumours are a product of complex systems. Governments cannot stop the rumours. Simply, we need to be in a position to shrug off rumours, be robust in the face of them.

8. Do not give an addict more drugs if he has withdrawal pains. Using leverage to cure the problems of too much leverage is not homeopathy, it is denial. The debt crisis is not a temporary problem, it is a structural one. We need rehab.

9. Citizens should not depend on financial assets or fallible “expert” advice for their retirement. Economic life should be definancialised. We should learn not to use markets as storehouses of value: they do not harbour the certainties that normal citizens require. Citizens should experience anxiety about their own businesses (which they control), not their investments (which they do not control).

10. Make an omelette with the broken eggs. Finally, this crisis cannot be fixed with makeshift repairs, no more than a boat with a rotten hull can be fixed with ad-hoc patches. We need to rebuild the hull with new (stronger) materials; we will have to remake the system before it does so itself. Let us move voluntarily into Capitalism 2.0 by helping what needs to be broken break on its own, converting debt into equity, marginalising the economics and business school establishments, shutting down the “Nobel” in economics, banning leveraged buyouts, putting bankers where they belong, clawing back the bonuses of those who got us here, and teaching people to navigate a world with fewer certainties.

Then we will see an economic life closer to our biological environment: smaller companies, richer ecology, no leverage. A world in which entrepreneurs, not bankers, take the risks and companies are born and die every day without making the news.

In other words, a place more resistant to black swans.

Happy November!

Scott Dauenhauer, CFP, MSFP, AIF

Saturday, October 30, 2010

Wednesday, October 27, 2010

Ordos, China: A Modern Ghost Town

Ordos, China: A Modern Ghost Town

Sorry, Central Planning doesn't work (did you hear that Bernanke).

Scott Dauenhauer, CFP, MSFP, AIF

Sorry, Central Planning doesn't work (did you hear that Bernanke).

Scott Dauenhauer, CFP, MSFP, AIF

Tuesday, October 26, 2010

Grantham on Gold

Religious wars (or, Should we buy gold?)

Everyone asks about gold. This is the irony: just as Jim Grant tells us (correctly) that we all have faith-based paper currencies backed by nothing, it is equally fair to say that gold is a faith-based metal. It pays no dividend, cannot be eaten, and is mostly used for nothing more useful than jewelry. I would say that anything of which 75% sits idly and expensively in bank vaults is, as a measure of value, only one step up from the Polynesian islands that attached value to certain well-known large rocks that were traded. But only one step up. I own some personally, but really more for amusement and speculation than for serious investing. It may well work and it may not. In the longer run, I believe that resources in the ground, forestry, agriculture, common stocks, and even real estate are more certain to resist any inflation or paper currency crisis than is gold.

I tend to agree with Jeremy.

Scott Dauenhauer, CFP, MSFP, AIF

Monday, October 25, 2010

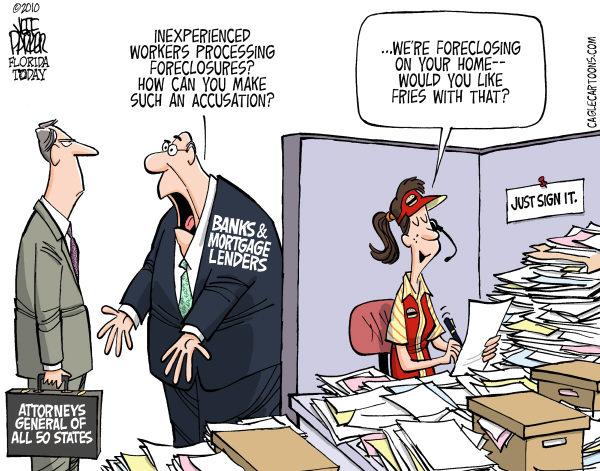

FDIC Fiasco: Bair backs "Safe Harbor"...as opposed to Rule of Law

In a mind-boggling appearance today Sheila Bair attempted to sweep the current foreclosure fiasco under the rug by backing a plan to allow a "safe harbor" for certain loans currently in foreclosure. In other words the banks would be allowed to foreclose if certain conditions are met....NOT if the bank has proven that they have the right to foreclose. The rule-of-law when it comes to foreclosures is being crushed and now the FDIC is all in with their buds over at Fannie and Freddie leading the charge.

Regardless of if a homeowner is able to pay or can afford to pay we have a system of laws that must be followed. We can't start making exceptions for large banks/services out of convenience, especially after the abuse that has been heaped upon this nation by the very same banks.

Bair's comments received almost no immediate press - which is remarkable.

Scott Dauenhauer CFP, MSFP, AIF

Regardless of if a homeowner is able to pay or can afford to pay we have a system of laws that must be followed. We can't start making exceptions for large banks/services out of convenience, especially after the abuse that has been heaped upon this nation by the very same banks.

Bair's comments received almost no immediate press - which is remarkable.

Scott Dauenhauer CFP, MSFP, AIF

Shilling: Home Prices Will Drop 20% More

This isn't surprising analysis from Gary Shilling, but it is very contrarian in nature.

Scott Dauenhauer, CFP, MSFP, AIF

Scott Dauenhauer, CFP, MSFP, AIF

PragCap: How To Beat The Market

Pragmatic Capitalist via Zero Hedge via Goldman Sachs:

Prag Cap:

“On the interplay between the FED and STOCKS: Since Sept 1 – when QE was becoming a mainstream focus – if you only owned S&P on days when the Fed conducted Open Market Operations (in US Treasuries), your cumulative return is over 11%. in addition, 6 of the 7 times when S&P rallied 1% or more, OMO was conducted that day. this compares to a YTD return of 5.8%. the point: you would have outperformed the market 2x by being long on just the 16 days when – this is the important part – you knew in advance that OMO was to be conducted. The market’s performance on the 19 non-OMO days: +70bps.”

Prag Cap:

The Fed certainly doesn’t help their credibility when this sort of stuff is being thrown in people’s faces. It’s one thing to imply that you’re going to print millions of dollars. It’s a whole other thing to admit that you want to run a ponzi economy (as Brian Sack directly did). Amazing way to run an economy….

Friday, October 22, 2010

Tuesday, October 19, 2010

Hussman on QE

From Jon Hussman:

Scott Dauenhauer, CFP, MSFP, AIF

Unfortunately, the likely economic impact of this rapid depreciation is not benign. The Fed might like to believe that a cheaper dollar will improve trade by increasing U.S. exports and reducing imports. However, over the past two decades, and particularly in recent years, U.S. imports have been much more elastic in response to fluctuations in the U.S. dollar than exports have been. This suggests that provoking further dollar depreciation is likely to have negative effects on the global economy, owing to a shift away from imports, but with few positive effects for U.S. economic activity. Indeed, a further depreciation would unnecessarily create a negative wealth effect for U.S. consumers facing higher prices for imported goods and services. Any improvement in the trade deficit would be largely offset by downward pressure on U.S. consumption.

As a side note, some observers have suggested that QE represents nothing more than "printing money." While this might be accurate if the Fed never reverses the transactions, the most useful way to think about QE, in my view, is as an attempt to directly lower interest rates by purchasing Treasury securities. This interest rate effect - not any major inflationary outcome - is the cause of the dollar depreciation we are observing here. There is little doubt that the effect of large continuing fiscal deficits is long-run inflationary, but as I've noted repeatedly over the years, there is little correlation between inflation and temporary - even large - variations in the monetary base. Inflation is ultimately a fiscal phenomenon born of unproductive spending, regardless of how that spending is financed.

Scott Dauenhauer, CFP, MSFP, AIF

Monday, October 18, 2010

3rd Quarter Commentary: Can You Print Your Way To Prosperity?

Can You Print Your Way To Prosperity?

The economy is not improving. While the NBER may have called the recession over as of last June - the one in five people who would like to have a job would beg to differ (data from Shadow Stats). I’ve stated on my blog and to many of you that I don’t believe we will have a Double-Dip Recession because we never recovered from the first one. The U.S. is stuck in the D gear - depression. Enter the Federal Reserve.

Last year the Federal Reserve embarked upon a program where it printed nearly $2 Trillion to buy Fannie/Freddie Mortgages and U.S. Treasuries. Combined with changes to accounting rules the market and numerous risk assets shot up, in some cases doubling. Since the money printing stopped earlier in the year stock returns haven’t even been up by 1%. In August the Federal Reserve decided to “keep the motor running” or “warm up the car” so to speak by reinvesting interest and mortgage pre-pays into longer-term U.S. Treasuries - effectively keeping the money supply constant (perhaps I should say the Reserves constant). All of this in a prelude to the next big event which many believe will happen at the November FOMC meeting, but could be pushed to the December meeting - Quantitative Easing 2.0. This simply means more money printing to buy Treasury bonds and potentially mortgages.

The belief that more money printing is on the way and that it is a solution to our economic woes has been witnessed on Wall Street. Stocks had their best September in 77 years and there are now economic commentators who believe you cannot lose in stocks - regardless of what the economy does. In fact, it has gotten so bad that now the Street is collectively hoping economic data is bad so that the Federal Reserve will follow through with its plan to print more money. In short, economic improvement is good for stocks - economic depression is even better for stocks. Anybody see anything wrong with this thought process? Less you think the Federal Reserve is the only Central Bank doing this, be forewarned that the Bank of Japan is now printing money to buy Exchange Traded Funds and Real Estate...is the U.S. next?

Stock prices are driven by short-term forces, but over the longer-term they are driven by valuations and stocks are not priced for superior or even average returns going forward. If the economy was devolving and stocks traded for 10 times earnings - I could be excited about the prospects for stocks, even if I wasn’t hopeful about the economy. At 20 times earnings stocks are priced for perfection, if anything goes wrong they will suffer.

The question is no longer whether we should print more money, but how much more should we print? We will likely find out soon, but it is now clear that low interest rates are here to stay - for a long time. The goal of the Fed is to get you to stop saving your money in banks, money markets and short-term instruments that yield next to nothing and instead use that money to speculate on more risky assets such as stocks, long-term bonds and anything that will get asset prices up. The goal is to boost asset prices so they can be sold off bank and other balance sheets - to some greater fool...guess who that fool is?

There is an old phrase - “Don’t fight the Fed” and it appears Wall Street is following it. But should you? The answer is no - you shouldn’t follow the adage - you SHOULD fight the Fed. You cannot print your way to prosperity. If you could, why would anybody produce anything? Why is there still hunger in the world if the solution is simply to fire up the printing press?

I don’t pretend to know the short-term implications of Federal Reserve short-term thinking, but my belief is that we are on the wrong path. The Federal Reserve, led by Ben Bernanke is leading us toward a cliff and instead of building a bridge most of the pundits have decided to strap on bunging gear and pray that the cord is connected...to something. If the term Lemmings comes to mind it is only because it is appropriate.

Investing in this environment will not be easy and returns will likely not be great (though I do not discount a stock boom, but believe if it happens it will bust). My strategy is to create as much flexibility as possible and take risks where appropriate. My advice to those saving for retirement is to continue saving as much as you can, for those in retirement it is to preserve your assets as much as possible.

While my quarterlies don’t appear to be getting any less gloomy, you might be surprised to hear that I am quite an optimist long-term. I believe the world is on the verge of scientific discovery that will literally make the past one-hundred years look like the stone ages. It will take some time, perhaps decades - but the advancements in bio-tech, medicine, technology, energy and education will be leaps - not steps. The one constant will be change (usually that phrase annoys me, but I believe it will be true). The changes that will take place likely won’t be easy and the immediate impact of such changes can’t be accurately gauged. If you think the iPad is cool (and I do) you haven’t seen anything yet - one day the iPad will be akin to an 8-track player. The problem we have now is that there are too many structural issues standing in the way of the global economy and these have to be worked out - but it takes time, lots of time and lots of pain. The future is bright, getting there may not be so.

Scott Dauenhauer, CFP, MSFP, AIF

The economy is not improving. While the NBER may have called the recession over as of last June - the one in five people who would like to have a job would beg to differ (data from Shadow Stats). I’ve stated on my blog and to many of you that I don’t believe we will have a Double-Dip Recession because we never recovered from the first one. The U.S. is stuck in the D gear - depression. Enter the Federal Reserve.

Last year the Federal Reserve embarked upon a program where it printed nearly $2 Trillion to buy Fannie/Freddie Mortgages and U.S. Treasuries. Combined with changes to accounting rules the market and numerous risk assets shot up, in some cases doubling. Since the money printing stopped earlier in the year stock returns haven’t even been up by 1%. In August the Federal Reserve decided to “keep the motor running” or “warm up the car” so to speak by reinvesting interest and mortgage pre-pays into longer-term U.S. Treasuries - effectively keeping the money supply constant (perhaps I should say the Reserves constant). All of this in a prelude to the next big event which many believe will happen at the November FOMC meeting, but could be pushed to the December meeting - Quantitative Easing 2.0. This simply means more money printing to buy Treasury bonds and potentially mortgages.

The belief that more money printing is on the way and that it is a solution to our economic woes has been witnessed on Wall Street. Stocks had their best September in 77 years and there are now economic commentators who believe you cannot lose in stocks - regardless of what the economy does. In fact, it has gotten so bad that now the Street is collectively hoping economic data is bad so that the Federal Reserve will follow through with its plan to print more money. In short, economic improvement is good for stocks - economic depression is even better for stocks. Anybody see anything wrong with this thought process? Less you think the Federal Reserve is the only Central Bank doing this, be forewarned that the Bank of Japan is now printing money to buy Exchange Traded Funds and Real Estate...is the U.S. next?

Stock prices are driven by short-term forces, but over the longer-term they are driven by valuations and stocks are not priced for superior or even average returns going forward. If the economy was devolving and stocks traded for 10 times earnings - I could be excited about the prospects for stocks, even if I wasn’t hopeful about the economy. At 20 times earnings stocks are priced for perfection, if anything goes wrong they will suffer.

The question is no longer whether we should print more money, but how much more should we print? We will likely find out soon, but it is now clear that low interest rates are here to stay - for a long time. The goal of the Fed is to get you to stop saving your money in banks, money markets and short-term instruments that yield next to nothing and instead use that money to speculate on more risky assets such as stocks, long-term bonds and anything that will get asset prices up. The goal is to boost asset prices so they can be sold off bank and other balance sheets - to some greater fool...guess who that fool is?

There is an old phrase - “Don’t fight the Fed” and it appears Wall Street is following it. But should you? The answer is no - you shouldn’t follow the adage - you SHOULD fight the Fed. You cannot print your way to prosperity. If you could, why would anybody produce anything? Why is there still hunger in the world if the solution is simply to fire up the printing press?

I don’t pretend to know the short-term implications of Federal Reserve short-term thinking, but my belief is that we are on the wrong path. The Federal Reserve, led by Ben Bernanke is leading us toward a cliff and instead of building a bridge most of the pundits have decided to strap on bunging gear and pray that the cord is connected...to something. If the term Lemmings comes to mind it is only because it is appropriate.

Investing in this environment will not be easy and returns will likely not be great (though I do not discount a stock boom, but believe if it happens it will bust). My strategy is to create as much flexibility as possible and take risks where appropriate. My advice to those saving for retirement is to continue saving as much as you can, for those in retirement it is to preserve your assets as much as possible.

While my quarterlies don’t appear to be getting any less gloomy, you might be surprised to hear that I am quite an optimist long-term. I believe the world is on the verge of scientific discovery that will literally make the past one-hundred years look like the stone ages. It will take some time, perhaps decades - but the advancements in bio-tech, medicine, technology, energy and education will be leaps - not steps. The one constant will be change (usually that phrase annoys me, but I believe it will be true). The changes that will take place likely won’t be easy and the immediate impact of such changes can’t be accurately gauged. If you think the iPad is cool (and I do) you haven’t seen anything yet - one day the iPad will be akin to an 8-track player. The problem we have now is that there are too many structural issues standing in the way of the global economy and these have to be worked out - but it takes time, lots of time and lots of pain. The future is bright, getting there may not be so.

Scott Dauenhauer, CFP, MSFP, AIF

Alt. Energy Update: Super Soaker Inventer To Revolutionize Solar Power?

My outlook might be gloomy in the short-intermediate term, but my long, long term via is, well bright. As I've said time and time again I believe we are on the brink of technological and biological developments on par with nothing that mankind has ever witnessed. Unfortunately this will take time, perhaps decades - which we must linger through. But along that theme is this incredible breakthrough for solar power, The Atlantic profiles Lonnie Johnson:

The key to the JTEC is the second law of thermodynamics. Simply put, the law says that temperature differences tend to even out—for instance, when a hot mug of coffee disperses its heat into the cool air of a room. As the heat levels of the mug and the room come into balance, there is a transfer of energy.

Work can be extracted from that transfer. The most common way of doing this is with some form of heat engine. A steam engine, for example, converts heat into electricity by using steam to spin a turbine. Steam engines—powered predominantly by coal, but also by natural gas, nuclear materials, and other fuels—generate 90 percent of all U.S. electricity. But though they have been refined over the centuries, most are still clanking, hissing, exhaust-spewing machines that rely on moving parts, and so are relatively inefficient and prone to mechanical breakdown.

Johnson’s latest JTEC prototype, which looks like a desktop model for a next-generation moonshine still, features two fuel-cell-like stacks, or chambers, filled with hydrogen gas and connected by steel tubes with round pressure gauges. Where a steam engine uses the heat generated by burning coal to create steam pressure and move mechanical elements, the JTEC uses heat (from the sun, for instance) to expand hydrogen atoms in one stack. The expanding atoms, each made up of a proton and an electron, split apart, and the freed electrons travel through an external circuit as electric current, charging a battery or performing some other useful work. Meanwhile the positively charged protons, also known as ions, squeeze through a specially designed proton-exchange membrane (one of the JTEC elements borrowed from fuel cells) and combine with the electrons on the other side, reconstituting the hydrogen, which is compressed and pumped back into the hot stack. As long as heat is supplied, the cycle continues indefinitely.

Oh, and he also invented the Super Soaker!

Scott Dauenhauer CFP, MSFP, AIF

RIP: Genius Mathematician Benoit Mandlebrot

Benoit Mandlebrot changed the way I think about everything, including Investing. His book "The (Mis)Behavior of Markets" was a clarion call to the investing community to view risk in more than just a single dimension - unfortunately it went unheeded. He is most famous for the theory of Fractal Geometry, which I won't attempt to explain but is a super important discovery. We will all miss Mandlebrot, but his ideas and influence will continue. It is my belief that his influence will continue to lead to incredible discoveries in math and science. RIP Benoit.

Tuesday, October 12, 2010

A Money Printing Analogy Courtesy of Art Cashin

Why Bernanke's Funny Money tricks won't work:

Thank you Art Cashin.

Scott Dauenhauer, CFP, MSFP, AIF

Every year as it begins to get cold in the northeast, oak trees drop acorns. The annual bounty helps countless squirrels, chipmunks, rabbits and other rodents endure the bitter winter months.

Let's say oak trees dropped 1.3 trillion acorns last winter and that an industrious squirrel hunted and gathered far more nuts than he needed. He sought to loan some to others, but the neighboring chipmunks and deer already had plenty. The Nuts, Acorns, and Seeds Administration, surveying the landscape, found the level of acorns unchanged at 1.3 trillion. Worried about another tough winter, it recommends that trees drop another 2 trillion acorns.

Thank you Art Cashin.

Scott Dauenhauer, CFP, MSFP, AIF

Monday, October 11, 2010

Friday, October 08, 2010

Why Are Distressed Homeowners Still Paying Their Mortgage?

Good Question - Interesting Answers - click above to read the opinion piece.

Scott Dauenhauer CFP, MSFP, AIF

Scott Dauenhauer CFP, MSFP, AIF

HR 3808 - Throw the Bums Out

If you ever needed a reason to get rid of an incumbent politician (Republican, Democrat or Otherwise) you now have one (yet another one). I try not to get political on this blog, but what we have witnessed over the past decade (or more) is the abdication of the people's interest for Wall Street/Big Banking's interests.

The finance industry has taken over this country, led by Ben Bernanke at the Federal Reserve and the death grip they have is strangling the poor and the middle class. Nowhere is this more prevalent than in Congress where our beloved (approval rating below 20%) politicians are either in the pockets of the banking industry or just plain stupid (please understand I am not ruling out the possibility that both may apply).

HR 3808 was authored by a Republican and co-sponsored by three Democrats and guess who voted for it? Nobody knows. That's right, there is no record of WHO voted for it as it was a Voice Vote in the House and done by Unanimous Consent in the Senate (a process which I don't fully understand). There was no public debate. This was a deliberate act of Congress to evade detection of a bill that would hurt Main Street and help the Banksters by making it easier to foreclose.

Congress doesn't even have the guts to put there name on the vote and now many members are coming out against it...when it scores them political points.

No politician that I am aware of led the fight to Kill the Bill - which means they implicitly wanted it or simply didn't read the bill - neither of which is acceptable.

This is a complete betrayal of the American people and Obama did the right thing by sending it back to Congress (as if he had a choice).

I'm not going to tell you how to vote - to be perfectly honest I don't know how to vote anymore, but trusting Congress to do the right thing is not something that I have within me.

Scott Dauenhauer, CFP, MSFP, AIF

The finance industry has taken over this country, led by Ben Bernanke at the Federal Reserve and the death grip they have is strangling the poor and the middle class. Nowhere is this more prevalent than in Congress where our beloved (approval rating below 20%) politicians are either in the pockets of the banking industry or just plain stupid (please understand I am not ruling out the possibility that both may apply).

HR 3808 was authored by a Republican and co-sponsored by three Democrats and guess who voted for it? Nobody knows. That's right, there is no record of WHO voted for it as it was a Voice Vote in the House and done by Unanimous Consent in the Senate (a process which I don't fully understand). There was no public debate. This was a deliberate act of Congress to evade detection of a bill that would hurt Main Street and help the Banksters by making it easier to foreclose.

Congress doesn't even have the guts to put there name on the vote and now many members are coming out against it...when it scores them political points.

No politician that I am aware of led the fight to Kill the Bill - which means they implicitly wanted it or simply didn't read the bill - neither of which is acceptable.

This is a complete betrayal of the American people and Obama did the right thing by sending it back to Congress (as if he had a choice).

I'm not going to tell you how to vote - to be perfectly honest I don't know how to vote anymore, but trusting Congress to do the right thing is not something that I have within me.

Scott Dauenhauer, CFP, MSFP, AIF

Wednesday, October 06, 2010

Schapiro got nearly $9M final payout from Finra - Investment News

Schapiro got nearly $9M final payout from Finra - Investment News

Current SEC Chairman received $9m in Final pay for leaving FINRA, this is ridiculous.

Scott Dauenhauer CFP, MSFP, AFI

Current SEC Chairman received $9m in Final pay for leaving FINRA, this is ridiculous.

Scott Dauenhauer CFP, MSFP, AFI

Saturday, October 02, 2010

Toxic Titles - The Spawn of Toxic Assets

First there were subprime loans which turned into Toxic Loans - now these Toxic Loans have spawned a whole new mess that is making national headlines - Toxic Titles. The Bloomberg article I link to above reports:

Essentially, millions of Titles (a title is what represents ownership) and current and prior Title transfers are at-risk because of sloppy paperwork and a system (MERS) that is increasingly being questioned by the courts as to whether or not it has standing.

The avalanche of disclosure this week (BofA, Chase, GMAC) that their foreclosure mills were not being run properly is but a symptom of the overall problem - Toxic Titles. If this situation is not resolved it quite literally threatens to invalidate millions of title transfers and with it, potentially trillions in value - essentially cratering the entire global economy.

Of course the powers that be would never allow this to happen, but a legal decision must be made and the courts are beginning to see the light on this issue. You can bet that the banks and Fannie/Freddie are fighting this hard and are running scared.

Scott Dauenhauer, CFP, MSFP, AIF

“A mortgage has to follow the proper trail every step of the way, or you have title problems,” he said.

In some cases, mortgages were conveyed using the Reston, Virginia-based Mortgage Electronic Registration System, or MERS, designed to cover transfers among system members. Promissory notes also often were endorsed as payable to the bearer to avoid the need for multiple transfers. Both practices have been challenged in court.

Copies of documents aren’t enough to establish rights, just as copies of dollar bills wouldn’t be honored by a bank, said Geoff Walsh, an attorney with the National Consumer Law Center in Boston. In cases of lost or mishandled paperwork, attorneys may file affidavits and other evidence to correct omissions and establish a claim, Walsh said.

“Wall Street was very good at packaging loans and making sure the money flowed to the right people, but not so good at keeping track of mortgage documents,” Engel said. As a result, “we have a growing number of toxic titles,” she said.

Essentially, millions of Titles (a title is what represents ownership) and current and prior Title transfers are at-risk because of sloppy paperwork and a system (MERS) that is increasingly being questioned by the courts as to whether or not it has standing.

The avalanche of disclosure this week (BofA, Chase, GMAC) that their foreclosure mills were not being run properly is but a symptom of the overall problem - Toxic Titles. If this situation is not resolved it quite literally threatens to invalidate millions of title transfers and with it, potentially trillions in value - essentially cratering the entire global economy.

Of course the powers that be would never allow this to happen, but a legal decision must be made and the courts are beginning to see the light on this issue. You can bet that the banks and Fannie/Freddie are fighting this hard and are running scared.

Scott Dauenhauer, CFP, MSFP, AIF

Friday, October 01, 2010

Secrets of the Wirehouse Repost

It’s been nearly five years since I wrote “Secrets of the Wirehouse” and I feel it is time to update it and add to it and sometimes subtract from it. You can read the original piece by clicking here. I encourage you visit my blog at http://themeridian.blogspot.com for updates on current financial events. Visit Scott’s website at www.meridianwealth.com.

Secrets of the Wirehouse

And How to Protect Your Best Interests

About the Author:

Scott Dauenhauer spent five years working for the “big three” brokerage’s and gained his knowledge first hand. He is now a Certified Financial Planner and has a Masters Degree in Financial Planning. Scott is the Owner and President of Meridian Wealth Management, a firm dedicated to protecting client interests. He believes in focusing on people not products. Though he believes there are some good people at brokerage firms, he thinks the vast majority fall extremely short of what is needed to advise a family on a subject as important as Financial Planning.

To find out more please visit his website: www.meridianwealth.com

Most Brokers Do Not Have Formal Training in Financial Planning

How much training do brokers actually have in financial planning? Major brokerage firms tout intensive training programs almost as much as the stocks they peddle. They brag about the high level of education their “consultants” receive. The truth is the only requirements are that individuals pass the Series 7, and a state insurance exam. The Series 7 is an industry test that requires memorization of facts about the markets and represents a minimum standard of knowledge.

The Series 7 does not teach an individual how to manage personal finances, let alone create a comprehensive financial plan. The Series 7 doesn’t even teach about how to properly diversify a portfolio. The insurance exam is an even bigger farce. While the Series 7 actually requires a bit of studying the state insurance exams only require minimal memorization. In California you are required to attend a 52 hour class in order to sit for your insurance exam. The class I took was excessively boring and did not teach anything about actual insurance policies or how to determine the proper amount of life insurance for an individual or family. Worst of all at the end of the 52 hour class the instructor gave you all the questions that would show up on the exam and the answers, almost word for word (I know, I took the exam and was shocked to see nearly the exact same questions).

The only thing they didn’t give you was what order the questions would be and whether the answer was a,b,c, or d. I would be willing to bet that by the time my son is 7 years old he could pass this exam. I think this is less a securities scandal and more a state governance scandal (the excuse by the state is that an easy test promotes more people in the insurance business and that the insurance companies will train the individuals……and you wonder why there is so much insurance fraud).

Anyway, once a “recruit” passes the Series 7, he/she is sent to company headquarters to go through “intensive training.” The training is definitely intensive, though not in financial planning or investment management. The programs focus solely on sales & product training and lasts anywhere from 1-4 weeks. I attended one such program and 95% of the training focused on cold-calling sales and learning proprietary product. Proprietary products are ones that are sold directly (and typically only) by the brokerage firm and typically have much higher profit margins, though mainly benefit the firm, not the person they are sold too. Brokerage firms want “salespeople,” not highly skilled financial planners.

If the firms hired highly skilled financial planners, the firm wouldn’t be able to sell proprietary products. This is because the planners would know better. When the firm hires somebody with no previous industry knowledge, or experience, they have the opportunity to fill that person’s mind with fairy tales, not fact. The firms’ way of doing business is to focus on proprietary products, high & hidden fees, cold calling, and quotas. The truth is that very few new recruits have any experience in handling another family’s wealth. You end up paying high fees for a service that puts you directly on a recruit’s learning curve. Even brokers who have been at the firm for years may not have any training in financial planning; they are stockbrokers, not trusted advisors.

As the years have gone by firms are moving slowly away from proprietary products, though not entirely. It would not be unusual to be sold a hedge fund, futures fund, or separate account, or variable annuity that is more all intents and purposes proprietary (despite a name that is different than the brokerage firms name).

Your advisor should have prior experience in financial planning and be Certified Financial Planner at a minimum, if not; you are putting your family’s wealth at risk. Please don’t let your finances be somebody else’s training ground.

Your Mutual Funds Are NOT Free

Mutual funds have grown into a huge industry. Once a small subset of money management, they have grown into a product that is now held by a large percentage of American households. There are now more mutual funds in the U.S. than stocks that trade on the NYSE. The proliferation of this medium of investing has empowered the individual investor. However, at the same time it has powered the Mutual Fund and Brokerage industry to record profits. Many of these companies are pulling the wool over your eyes. Most investors do not understand the fees accessed in their mutual fund. Even “no-load” funds have expenses. Though most of the costs are disclosed in the prospectus (good luck deciphering), some are not.

You will never see a bill for your mutual fund because the expenses are hidden. They may be hidden, but believe me, they exist. There are four major expenses involved with mutual funds (and a few minor ones). The first expense is the Expense Ratio; this compensates the manager, analysts, board of directors, and pays printing, mailing, & overhead costs and ranges from .20% to 2.0% annually. The average is about 1.5%. The next cost is what the industry refers to as a 12b-1 fee; this is basically a hidden commission. The 12b-1 fee pays to bring in new shareholders and has zero benefit to you. It varies depending on what share-class is sold to you and runs from .25% to 1.0% annually.

The last two expenses are not actually printed anywhere, you have to calculate them yourself. These expenses are spread/impact costs and transaction expenses. Every time your mutual fund buys and sells stock there are costs. The more a fund trades the more expenses YOU incur. In November of 2004 a study was released by the Zero Alpha Group (click here for the study) that stated “U.S. investors in equity mutual funds are paying $17.3 billion in hidden mutual fund trading costs that are not reported openly in the stated expense ratios of mutual funds.” The study found that on average brokerage commissions add .38% to a funds annual expense and trading costs (spreads & market impact) add another .58%. The study also found that these costs are much higher for small stock funds than large stock funds. On a conservative basis most mutual funds have additional undisclosed costs that total nearly 1% and in many circumstances higher.

Another cost you do not see is what John Bogle refers to as the “cash drag factor,” basically most mutual funds are not fully invested, they keep anywhere from 1-10% cash on hand. This hurts the performance on the upside but cushions it on the downside, since the market has gone up more often than down, the cash in the fund brings down the performance. Bogle estimates it to be about .6% on the high end. Let’s add up all the potential costs of a mutual fund, keeping in mind that brokerage firms are known for being on the high end.

Passive Low End Active Normal

Cash Drag 0% .60%

Expense Ratio .20% 1.33%

12b –1 Fee’s 0% 1.00%

Trading Costs .06% 1.00%

Total Costs .26% - 3.96%

The low end cost represents a person not receiving any advice; a typical fee for a professional advisor is .75% of assets annually bringing the total low end cost to around 1.00%. Not all broker sold funds have costs that are as high as shown above, however the average is somewhere between 2 - 3% annually.

Does your broker have your best interests in mind when he is charging you 2 – 4 times what a professional competent financial planner might charge? I would argue not.

Conflicts of Interest Abound – More Strings Attached Than A Marionette Puppet

Conflicts of interest exist in almost any business, the mere presence of a conflict does not automatically lead to a persons interests being wrongfully represented. However, all conflicts that are known should be disclosed in writing to the potential client before a relationship starts.

When dealing with brokerage firm conflicts of interest abound and for the most part are not disclosed. The following is a few conflicts that you should watch out for.

First, please understand to whom a public company owes their loyalty; it is to their public shareholders. The people who own stock in a company must have their interests protected. A public brokerage firm’s loyalty cannot be 100% to you.

Let’s take a further look at where other strings are attached. A broker gets paid a percentage of the revenues that he/she brings to the firm, typically 25-40%. It is not, however, that simple. Brokerage firms determine the payout percentage for each individual “product.” They control product flow by paying higher amounts to brokers for product they want sold (typically products with higher margins). While this makes sense from a business stand point and from a shareholder standpoint (why wouldn’t you want to incentivise your staff to sell the most profitable products?) it doesn’t work out so well for the end user, the client. Each firm works differently but depending on the product a firm wants to emphasize, they will pay a broker a higher percentage of the revenue to induce him to sell what the company wants him to sell. For example, if the company wants a broker to sell a Separate Account Platform product (individual money managers, more to come on this), they may tell the broker that they will receive a higher percentage of the fees they generate from that particular product and that product may generate more fees than other products.

Let me give you a real life example so that you understand.

Imagine that you had only two products to choose from to sell your client; one is a mutual fund that costs the client 2.25% annually and pays the firm 1% annually. Of the 1% paid to the firm the broker collects 35% of it or .35% annually. On a $1,000,000 account the firm generates $10,000 in revenue and pays the broker $3,500 (you the client pay $22,500). The other product is a Separate Account where you have an individual money manager. This product is sold as the latest, greatest way to have your money managed and costs 2.5% annually. However, this product pays the firm 1.5% annually and the firm will pay the broker 40% of that revenue or .60% annually. On the same $1,000,000 account the firm generates $15,000 in revenue and pays the broker $6,000 (you pay $25,000 annually). Now, in all likelihood both accounts will have similar returns over time and will probably under-perform the market. You the client in either situation are stuck in a lousy product that is expensive; however the firm has an incentive to sell one over the other, even if the other isn’t in your best interest. The separate account sale earns the firm 50% more revenue and the broker 70% more revenue – which product do you think will be presented? Each firm has their own system and they are all different, but the mechanisms are in place to manipulate the broker into selling what makes the firm and/or the broker more money.

In 2000 I wrote the following:

“A more blatant conflict is a practice that people thought was eliminated a long time ago. Some brokerage firms pay their brokers more for selling proprietary (company managed) mutual funds. To be fair, most firms have eliminated this practice, to which I applaud them, however there is still at least one major brokerage firm that sill pays brokers up to 25% more commissions to sell their company managed mutual funds over other competing funds. In addition, the more company managed funds a broker sells, the more perks they receive. Whether it is a trip, an expense account, or personal gifts, they do not receive these perks if they sell other companies funds.”

The firm I was referring to at the time was Morgan Stanley Dean Witter (now Morgan Stanley) and I don’t know if they still pay more for in house funds, but I do know that they got into a lot of trouble with the New York Attorney General and the Securities and Exchange Commission for using the allure of trips and other incentives to sell funds that they had special arrangements with. Morgan Stanley was fined $50 million, though I doubt they’ve learned their lesson. I reported on all of this going on back in 2000 before Eliot Spitzer and his gang tackled Morgan and much of the industry.

The other mutual fund scandal that was uncovered that wasn’t news to me (or anyone in the industry) was the “shelf space” arrangement. This is your basic pay to play arrangement. Certain mutual fund companies receive more access to brokers to sell their funds and more attention is paid to these funds in exchange for a basic kickback on all sales made in that fund forever. The basic system would be that a fund company could get on a brokerage firms “Preferred List” by promising to make certain “revenue-sharing” arrangements with the brokerage firm. These revenue sharing arrangements many times were simply kickbacks paid for being on the preferred list and receiving preferred access. Mutual fund companies didn’t get on a preferred list because they were the best in their class, but because they paid more than another fund company might be willing to pay. Thus the client is more apt to be recommended a fund from the preferred list even if it isn’t the best fund. Despite large fines and penalties and lots of bad press this practice continues, but at least it is now disclosed on brokerage firm websites (though I would venture to guess you’ll never hear about it from your broker). To see Morgan Stanley’s lengthy disclosure click here.

In addition to higher revenue on proprietary products, the broker many times is under tremendous pressure from management to sell you the latest mutual fund offering from that brokerage. Branch manager compensation is determined in part by the amount of proprietary products his branch sells. His interest is in getting the highest bonus possible, so he in turn puts the pressure on the brokers to “pound the phones,” and sell their “latest offering.” The brokers are enticed by management with trips, dinners, and a host of other items. It goes unspoken that if a broker does not participate in selling the new offering then things will not be easy for him/her. I know of one broker who was told, “I don’t think this firm is the right place for you,” after the broker refused to sell the new fund offering. It turned out that he was the only one to not succumb to the pressure, he eventually left that firm. I can’t begin to tell you how many voice mails & e-mails I received from management to ‘sell’ the “new” offerings, I never succumbed because it was not in my client’s best interest. Be aware that the pressure is on your broker to sell certain products or else he/she risks losing their job.

The Broker Food Chain

Guess how many entities get paid on your mutual fund purchase? You’d be astonished.

O.K., we’ve established that you pay higher costs to work with an advisor at a major brokerage firm. But who actually receives the fees that your mutual funds, and managed accounts generate? You wouldn’t believe all the entities that must be paid from your simple purchase. Most investors believe 100% of the expenses or fees go directly to the broker. Actually a very small percentage actually ends up in your broker’s pocket (which must make you also question the intelligence of your broker). In most cases the portion of the fee that the broker receives is 25-40% of the revenues your account generates for the firm. If this sounds confusing, it is, most brokers don’t even understand their own pay structures (which is exactly what the firm wants).

To help you understand, let’s take a look at a mutual fund. A typical broker sold mutual fund will have total expenses of about 2 - 4%. As I showed you in the earlier example on a mutual fund the firm might generate $10,000 on a $1,000,000 account (annually). Of the $10,000 the broker might get paid $3,500 (.35%). So where does the rest go?

It goes to pay for the fancy office, the mutual fund manager, branch manager, profits, internal departments, performance reporting, analysts, wholesalers, and a myriad of other things. Don’t get me wrong, I don’t believe profit is a dirty word; however there is a difference between profit and gouging. Your costs are high because there are so many people and departments and corporations that must receive a portion of your fees.

Let me break down the food chain for you. A person referred to as a wholesaler supports your broker, the wholesaler is the person who sells products to your broker from his/her mutual fund company. The mutual fund that employs the wholesaler also employs your fund manager and analysts to support him/her. The fund must also pay to transact business (although this cost is passed onto you, though not disclosed). The fund company and the brokerage firm must then pass along profits to it shareholders by either a higher stock price or dividends. As you can see, there are more entities getting paid on your mutual fund than you can count on one hand. I call this the Broker Food Chain. Your mutual fund purchases must make a lot of entities a profit, your broker, your brokerage firm, and the fund company, the question remains whether or not you get any profit? The broker food chain does not work in your best interest.

Insurance costs! What Your Broker Doesn’t Disclose About Their Commissions

Did you know that your stockbroker or advisor at your major brokerage firm now sells insurance? That’s right, everything from Term life to Long Term Care. Most brokers got their insurance license so they could sell you annuities (we will get to that next); they discovered however that commissions are much more lucrative in insurance than anything else. So are you to believe that your broker is now an expert in matters of insurance? Don’t believe it. Unless he/she has been through special programs like the CFP, CLU, or CHFC, they may not be qualified to offer you advice; of course that does not stop them. Of the three the CLU is the by far the strongest mark for insurance. Insurance is a complex world and if purchased incorrectly it can do a lot of harm to you and your estate.

Commissions can run anywhere from 50-120% of your policies first year premium. Surprised, don’t be, they’ve always been that high. Actually, it’s not the commission that really upsets me. If a professional does his/her job correctly and has the knowledge, training, & expertise and makes an unbiased recommendation than the commission can be justified. The problem I have is with disclosure, or rather the lack there of. Very rarely will your broker disclose what he/she is being compensated or about the potential surrender charges. The other problem I have is that many times the broker will see commissions and the appropriateness of the product as separate decisions, giving more weight to the commission than the appropriateness of the product. Many times this is done in haste because the broker simply doesn’t understand what is or isn’t appropriate. Most brokers receive sales & product training, not financial & wealth management training. In most cases your broker is a marketing representative for a large publicly traded company, not a trusted advisor like they claim.

In addition, brokers cannot go out into the marketplace and choose any provider for insurance, they must stick with pre-approved “preferred” insurance providers, well, we already know what it takes to become “preferred” at a brokerage firm, don’t expect your best insurance interest to be looked after at a brokerage firm.

Annuities, Hazardous to Your Wealth?

Annuities are an interesting product. They come in all sizes, shapes, and forms. You have probably heard of both fixed & variable annuities. Fixed annuities pay a fixed interest rate as stated in the contract for a specific time period (similar to a CD). Variable annuities performance is based on an underlying “sub-account,” basically a mutual fund. The major benefit to an annuity is the ability to defer taxes until the money is withdrawn. Another highly touted benefit is that an annuity can pay an income stream for life. Let me lay out a case for why variable annuities may be hazardous to your wealth.

It has always been said that annuities are “sold,” not bought by investors. Over 90% of all annuity sales are through brokers or life agents, a viable no-load Variable annuity industry has not emerged. Why are so many people sold annuities? The answer is simple…. high commissions and great sounding stories. There are some annuities that brokers sell that pay the broker in excess of 10% commission (though this is mainly in reference to Equity Index Annuities, another topic). This leaves you with an expensive policy and surrender charges that may last more than a decade. The expenses inside an annuity are one of the main problems. There are several expenses involved. Today most annuities do not charge you an upfront commission, the fee is charged as an annual fee (which you don’t see). This fee is deducted daily from your balance, there are five possible costs. The costs are: The policy charge, Mortality & Expense, Rider charges, underlying sub-account expenses, & transaction costs associated with those sub-accounts. Below is a range of what these cost can add up to:

Policy Charges - $30-50

M & E - 1.0 – 2.0%

Riders - .25 – 1.25%

Sub-Accounts - .25 – 1.50%

Turnover costs - .06 – 1.00%

Total Costs - 1.56 – 5.75% annually

The average cost runs about 2.5 – 4% a year. These expenses take a toll on the ability of the portfolio to match, or even beat the market. The annuity has to earn 2.5-5% before it breaks even for the year. Add the fact that gains in an annuity are taxed as ordinary income when withdrawn and the chances of your annuity beating your taxable account come close to zero. In addition, if you die with an annuity you do not receive any favorable tax consequences. You lose what the tax code refers to as the “step-up” in basis, meaning that if you die with a taxable account the entire account gets passed on to your heirs with no income or capital gains tax, not so with an annuity. Studies have shown that even low cost annuities do not produce tax benefits big enough to beat an index fund in a taxable account. In a taxable account you receive a tax break if you hold your fund or stock for one year or more, not so with an annuity (plus dividends are now only taxed at 15% on the federal level, though this is set to expire). Lastly, you have very limited choice of investments in the annuities and if you want to take your money out before age 59 ½ you are out of luck, you would owe a 10% tax penalty.

You may ask “what about the guaranteed death benefit?” It is basically worthless in most circumstance. Annuities are long-term investments, they are not meant for periods of less than 10 years. If you end up being one of those poor unfortunate souls that bought at the top of the stock market and still have less money than you started with 10 years ago (extremely unlikely, but it happens, though usually do to idiot broker advice) then your loss exposure is likely minimal. An amount that will be less than what you probably paid for the insurance over that period. In any event, the death benefit is not a logical reason to purchase an annuity. The death benefit in an annuity is also rather inconvenient in that in order to collect you must DIE. I don’t know about you, but that is one “benefit” that doesn’t benefit me. Now, of course, if you have loved ones that you want to provide for a death benefit may offer you some peace of mind. Keep in mind what you pay for that peace of mind and the likelihood of it ever being collected on. If you are insurable purchase insurance, if you are not, perhaps a variable annuity with a death benefit makes sense (though I still highly doubt it). If in the extremely rare circumstance that a death benefit makes sense in a variable annuity my choice would be to purchase a variable annuity from the Vanguard Group, they offer a low cost account with a death benefit.

Let’s recap the problems with Variable Annuities. High expense, high marketing costs, tax penalties if under 59 ½, loss of capital gains status, loss of step-up, limited choice of investment vehicles, & worthless death benefits. So why do people continue to be sold these products? High commissions and high profitability to the companies involved. Profit is the bottom line, not your interests. Variable annuities have become such a problem that the SEC (regulator) has issued a booklet available online through its website www.sec.gov. that lists the pros and cons of annuities. In addition they are in the process of taking legal action against several major companies and brokers over selling tax-deferred annuities to people whom already have tax deferred accounts.

Living Benefits