I've been watching the congressional witch hunt of Tim Geithner this morning and in some ways feel sorry for him. Of course I still think he should be fired. In Geithner's mind he did what he thought was the right thing, he sees himself as a hero. I think he believes that his actions should not be questioned, in fact they should and in fact the actions of Geithner and his buddies was not right.

Goldman Sachs is also, probably rightly so, getting clobbered in the hearings. Its almost funny to see these politicians twisting questions just to mention the AIG name.

What is the most absurd thing to watch however is this gang of congresspeople attacking, but not taking any responsibility for their own actions. Geithner should resign, of course so should each of the people questioning him today.

The financial meltdown was not due to AIG alone. As I've said before, AIG basically did the same thing that Fannie and Freddie currently do - insured mortgages.

We need to get to the bottom of things, but when the people investigating need to be investigated themselves - we get nowhere. Geithner will be the fall guy, as he should be and hopefully Bernanke will be as well - they both need to go, but so does most of Congress.

Scott Dauenhauer CFP, MSFP, AIF

Wednesday, January 27, 2010

Tuesday, January 26, 2010

Asness & Grantham: Two Views

What follows are two different newsletters from people who seem to have opposite views, but are actually saying the same thing - Too Big Too Fail is the problem that needs to be fixed.

First Jeremy Grantham:

GMO January

Now Cliff Asness:

Appalled in Greenwich Connecticut 012610

First Jeremy Grantham:

GMO January

Now Cliff Asness:

Appalled in Greenwich Connecticut 012610

My 700th Post (Five years): Mauldin/Andy Miller - An Insiders View of the Real Estate Train Wreck

Perhaps one of the scariest articles you'll read, this is an interview with Andy Miller, a guy who called the top in Real Estate (both Residential and Commercial), here are few excerpts:

I've been saying many of the same things for the last year.

Scott Dauenhauer CFP, MSFP, AIF

Back in 2007, however, what most intrigued me about Andy was that he had been almost alone among his peer group in foreseeing the coming end of the real estate bubble, and in liquidating essentially all of his considerable portfolio of projects near the top. There are people that think they know what's going on, and those who actually know – Andy very much belongs in the latter category.

For all intents and purposes, the United States home mortgage market has been nationalized without anybody noticing. Last September, reportedly over 95% of all new loans for single-family homes in the U.S. were made with federal assistance, either through Fannie Mae and the implied guarantee, or Freddie Mac, or through the FHA.

If it's true that most of the financing in the single-family home market is being facilitated by government guarantees, that should make everybody very, very concerned. If government support goes away, and it will go away, where will that leave the home market? It leaves you with a catastrophe, because private lenders for single-family homes are nervous. Lenders that are still lending are reverting to 75% to 80% loan to value. But that doesn't help a homeowner whose property is worth less than the mortgage. So when the supply of government-facilitated loans dries up, it's going to put the home market in a very, very bad place.

In November, the FDIC circulated new guidelines for bank regulators to streamline and standardize the way banks are examined. One standout feature is that as long as a bank has evaluated the borrower and the asset behind a loan, if they are convinced the borrower can repay the loan, even if they go into a workout with the borrower, the bank does not have to reserve for the loan. The bank doesn't have to take any hit against its capital, so if the collateral all of a sudden sinks to 50% of the loan balance, the bank still does not have to take any sort of write-down. That obviously allows banks to just sit on weak assets instead of liquidating them or trying to raise more capital.

That's very significant. It means the FDIC and the Treasury Department have decided that rather than see 1,000 or 2,000 banks go under and then create another RTC to sift through all the bad assets, they'll let the banking system warehouse the bad assets. Their plan is to leave the assets in place, and then, when the market changes, let the banks deal with them. Now, that's horribly destructive.

Of course, very few people agree with that, because if you let it all go today, there would be enormous losses and a tremendous amount of pain. We're going to have some really terrible, terrible years ahead of us because letting it all go is the only way to be done with the problem.

I've been saying many of the same things for the last year.

Scott Dauenhauer CFP, MSFP, AIF

Economics In One Lesson: Fear the Boom and Bust

This is a pretty funny rap video pitting F.A. Hayek against John Maynard Keynes explaining each views on how economies work. I thought it was very funny, but I'm a finance geek. If you don't find it funny, I think you'll at least find it entertaining and hopefully educational.

Scott Dauenhauer CFP, MSFP, AIF

Scott Dauenhauer CFP, MSFP, AIF

Flashback: Meridian on Volcker

9/21/2009 - "I do not support Bernanke for Federal Reserve Chairman, maybe we should bring back Volcker!"

10/22/2009 - I posted an article featuring Paul Volcker and his reform policies, basically endorsing them

12/11/2009 - "It feels ironic to me that Paul Volcker is once again the voice of reason and sanity and yet he seems to be ignored in favor of Bernanke, Geithner, Dodd and Frank. Will it be the irony of ironies that the window dressing (Volcker) is in fact the one person in this administration that people should be listening too? I'm not saying we should rename Volcker to the Fed, but certainly getting rid of Geithner and replacing Bernanke would be wise moves."

I've been behind Paul Volcker since he started his campaign, its nice to see Obama finally listening to the one person in his administration that makes sense. While it would shake up markets in the short term and make a lot of people on Wall Street very unhappy I think that Obama's next move should be to ask Bernanke and Geithner to resign. He should use his bully pulpit to help fix the financial system (his bank tax is a populist ploy that I disagree with), this will give him the breathing room he needs to run for re-election. This should have been his first order of business.

I also think we've got to stop acting as if Wall Street was solely to blame for the crisis, it wasn't. What has really made people mad is the manner in which Wall Street and the banks have acted since the bailouts - with arrogance and hubris. We have to realize the problems were much greater than Wall Street - it encompassed our government and the Federal Reserve (the fourth branch). Wall Street certainly played its role, but didn't we all? It seems to me that the taxi driver earning $30,000 a year knew that he could not afford an $800,000 home, but signed on the dotted line anyway.

As I stated, Volcker's plans are a first step and we need to debate the issues and make the appropriate changes. I hardly believe that Obama was listening to me telling him to listen to Volcker (who seemed out in the wilderness for awhile), but I'm glad somebody finally got him to listen to the one voice of reason in his administration.

Scott Dauenhauer CFP, MSFP, AIF

10/22/2009 - I posted an article featuring Paul Volcker and his reform policies, basically endorsing them

12/11/2009 - "It feels ironic to me that Paul Volcker is once again the voice of reason and sanity and yet he seems to be ignored in favor of Bernanke, Geithner, Dodd and Frank. Will it be the irony of ironies that the window dressing (Volcker) is in fact the one person in this administration that people should be listening too? I'm not saying we should rename Volcker to the Fed, but certainly getting rid of Geithner and replacing Bernanke would be wise moves."

I've been behind Paul Volcker since he started his campaign, its nice to see Obama finally listening to the one person in his administration that makes sense. While it would shake up markets in the short term and make a lot of people on Wall Street very unhappy I think that Obama's next move should be to ask Bernanke and Geithner to resign. He should use his bully pulpit to help fix the financial system (his bank tax is a populist ploy that I disagree with), this will give him the breathing room he needs to run for re-election. This should have been his first order of business.

I also think we've got to stop acting as if Wall Street was solely to blame for the crisis, it wasn't. What has really made people mad is the manner in which Wall Street and the banks have acted since the bailouts - with arrogance and hubris. We have to realize the problems were much greater than Wall Street - it encompassed our government and the Federal Reserve (the fourth branch). Wall Street certainly played its role, but didn't we all? It seems to me that the taxi driver earning $30,000 a year knew that he could not afford an $800,000 home, but signed on the dotted line anyway.

As I stated, Volcker's plans are a first step and we need to debate the issues and make the appropriate changes. I hardly believe that Obama was listening to me telling him to listen to Volcker (who seemed out in the wilderness for awhile), but I'm glad somebody finally got him to listen to the one voice of reason in his administration.

Scott Dauenhauer CFP, MSFP, AIF

Friday, January 22, 2010

Simon Johnson: Obama’s Plan to Be Judged by a Goldman Breakup

A brilliant piece by MIT Professor Simon Johnson about the new Obama bank plan. As I've stated in a previous post I think this latest plan, while lacking on details and poorly presented (in terms of timing and meat on the bone) is generally a step in the right direction. It does not however solve the issues that found us in an ever tighter bust-boom cycle. For the first time since the president took office he has taken a positive step forward on the economy, of course it has not been met with much glee and Wall Street is throwing a hissy fit and gearing up their lobbyist to defeat any plan that might limit their power. How Obama and the Congress deal with this and other important issues regarding our financial system will determine whether the future course of our nation is one of prosperity or doom.

Of course regardless of if any financial reform is undertaken or not, if we don't stop our massive deficits, nothing else will eventually matter. Republicans have a chance to redeem themselves with the American people by helping to vote down Ben Bernanke and then joining with Obama on real financial reform. If they instead decide to oppose simply based on being the opposition party, while they may win a short-term victory, they will have doomed themselves and their party forever. I could care less about "bi-partisanship", its time each and every congressperson stepped up to the plate and delivered for the American people. I have little faith this will happen, but at least it can be said they were given a second chance before getting the boot (that goes for both parties).

Scott Dauenhauer CFP, MSFP, AIF

2010 Report Commentary

I'm posting this early even though I have not fully edited it given the recent market volatility. I was planning on finishing the editing and mailing out before month end, but figured now is a good time to get the information out to my clients, my edits will come later (so forgive the grammar) and in your mailbox (if you're a client).

Scott

Margin of Safety, Hyperinflation, Deflation and Experts

The Lost Decade

As we start a new decade and leave behind a “lost one” (is it ironic that the TV show Lost became a hit this last decade?), many are wondering how they should position their money for the future. The answer as always is not so simple, but my purpose here is to provide a framework for how I have come to the decisions for my clients portfolios going forward.

A lot has happened in the past eighteen months, we’ve seen spectacular losses and spectacular gains. A lot has also changed, much of it for the worse, though you wouldn’t know it by the gains in the stock market. One thing that is clear is that the stock market continues to be a very volatile place to put one’s money and volatility is not your friend in retirement. While things appear to have returned to normal, all is not well and in my opinion their is more risk than potential return in the stock markets (generally).

Margin of Safety

Warren Buffet and Benjamin Graham preach(ed) that one should obtain a “margin of safety” when purchasing any asset. The reasoning being is that things can and do go wrong and if you include a cushion, you (or the asset) can survive. This concept is why home lenders used to require a down payment of 20 - 30% - if real estate prices became depressed the lender would still have a cushion to soften the blow in the event of a default. The same concept applies when you are driving a car, the faster you are driving the further distance you should keep from the vehicle in front of you in case that car does something unexpected. We’ve become a society of “margin-less asset purchasers” or MAP’s for short. We buy something regardless of price with the “hope” of selling to a greater fool should prices begin to fall, however at that point in time the greater fool doesn’t exist to sell to.

The Tens Aren’t the Eighties

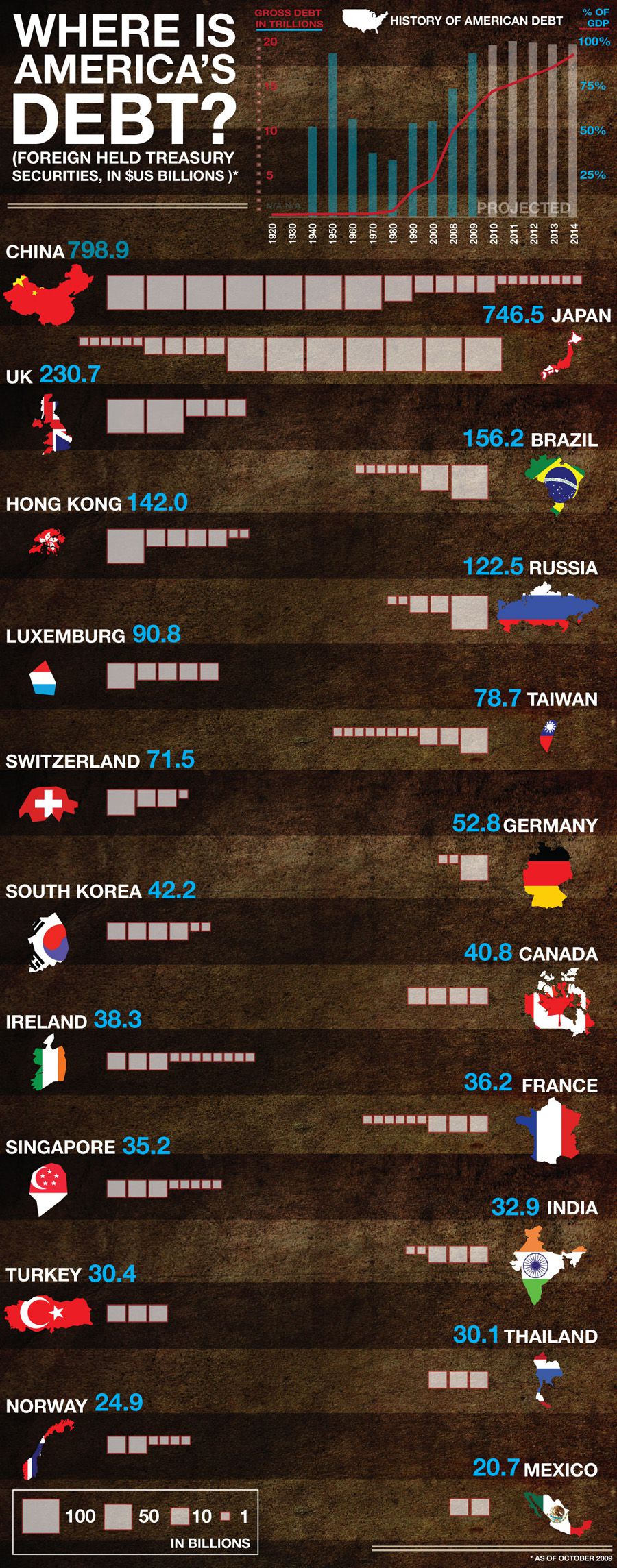

Many have compared today’s market environment to the early 80’s and contend we are at the beginning of another great boom for stock prices, yet this thinking ignores many differences between then and now. Back in 1980 we had less than $1 Trillion in national debt (in terms of GDP less than half of today), almost exclusively held by Americans (in one form or another), a billion was a lot of money even back then. Today our national debt is approaching $13 trillion and will likely be $14 Trillion sometime in 2011. This does not include entitlement debt which has a present value north of $60 Trillion, nor does it include municipal or personal debt.

Back in the 80’s we began running deficits and we have never looked backed (no we did not ever have a balanced budget during the Clinton years, that was an accounting trick). We will never again be able to balance the budget, it is not possible and we may be stuck with a budget deficit of close to $2 Trillion annually for many, many years.

Back in 1980 the trailing ten-year average P/E Ratio (a measure of stock valuation, the lower the ratio the lower the value) on the stock market was about 8, today it is over 20 (close to where it was in October 2007, before the crash started). Back in the 80’s states and municipalities were not nearly as leveraged as they are today. Currently unemployment is running close to 22% according to ShadowStats.com. Housing is not fixed, in fact we are facing a foreclosure crisis worse than we faced just last year as an avalanche of option-ARM mortgage are set to adjust and as the four government programs set up to stop foreclosure have failed miserably. Banks are allowed to borrow at next to nothing from the Federal Reserve and invest in risk-free treasury bonds earning a nice spread while ignoring small business who need access to credit. The housing market is being propped up by the government in a manner never before witnessed in the United States, they have attacked on four fronts:

FHA continues to make loans with little or nothing down to people with less than perfect credit

The Congress passed a law that gives free money (up to $8000) to people who buy a home.

The Federal Reserve embarked on a program that doesn’t appear to be legal to print money to buy mortgage backed securities of Fannie and Freddie (government controlled mortgage agencies) in order to push down interest rates for borrowers and new home buyers.

Finally, accounting rules have been relaxed in order to allow mortgages to be carried on bank balance sheets at essentially whatever the banks want, thereby making insolvent institutions look solvent and delaying the purge in homes that are delinquent.

This never before attempted government intervention in housing has kept housing from falling further and even helped prices in certain areas, though new home sales have yet to recover and high-end homes are having severe issues. Fixing housing has not been a priority, pumping it back up has been the order of the day, but it won’t work. I contend that unless housing is fixed we won’t have a meaningful recovery. This doesn’t mean we won’t have a recovery or that stock prices won’t go ever higher. The coming resets in Option-ARM mortgages will peak once in 2010 and again in 2011, these peaks will rival the sub-prime mortgage peaks and if not dealt with properly will pose a major headwind for real-estate and all other things financial.

In my opinion there are several things that need to be done in order to fix our financial system.

First, we must reinstate some version of Glass-Steagal, the Great Depression era law that essentially separated investment banks from commercial banking.

Second, we must separate out the risk taking hedge-fund like trading from the investment banks. The investment banks have leveraged themselves up to the point that if they are wrong on their speculations they could bring down our entire financial system, yet we continue to allow them to exist with an implicit guarantee that we will bail them out if they get it wrong. This allows them to borrow at lower interest rates as investors believe they will be defended by the government in the event of a blowup. This hurts competition as the government essentially provides a subsidy to one set of financial institutions, those that get big enough.

Third, we must remove the doctrine of Too-Big-Too-Fail, allowing institutions that take on to much risk and get it wrong to fail. Taxpayers should not be on the hook for losses that should be taken by stock and bondholders. The TBTF doctrine has failed and its the taxpayers who are paying the price all while those who benefit (Wall Street) take home massive, record bonuses. This is not only morally reprehensible, it is bad economics.

Fourth, in implementing Too-Big-Too-Fail we must breakup many of the large banks (Citibank, BofA, etc) and reduce the amount of FDIC insurance that is provided. Smaller institutions provide more competition and if regulated properly will not be able to take on the leverage and poorly underwritten assets that the large banks have purchased.

Fifth, we must reign in the Federal Reserve. The Fed has done more to devalue our currency than most understand. Since the creation of the Fed the dollar has fallen over 95% in value. While the Fed has been credited with saving the economy (Bernanke was named Time Man of the Year), it is more likely he has simply delayed the inevitable and made things much worse.

Sixth, we must fix housing. There are several solutions, some that include taxpayer money, others that don’t. We should make economically sound financial decisions like offering Principal Reductions when it makes sense to do so. John Hussman of the Hussman Funds has also come up with a system to deal rationally with this problem. This is essential.

Seventh, we must fix our entitlement problem (medicare, medicaid, social security). Our total national debt including entitlements is nearing $120 Trillion, of this over $100 Trillion is the present value of the short fall in Social Security and Medicare (Part D included). Did you know that Medicare Part D, which was just passed into law a few years ago under the Bush Administration already has a present value deficit greater than that of Social Security?

Eighth, we need to regulate Credit Default Swaps and make the system more transparent.

Implementing the above fixes will be politically difficult given the enormous amount of money that finances the campaigns of our politicians, but without these reforms and others we are destined to be on a boom-bust cycle for decades or be thrust into a greater depression than we are in currently. In addition, it is many of the current politicians that have created much of the chaos by passing budgets that are unsustainable. This is not unique to one-party. Perhaps throwing the bums out and starting over should be number one on my list above.

Experts

At this point you are probably wishing you hadn’t read this commentary, you might think I’m overly pessimistic and that perhaps I’ve thrown in with the crazies. I assure you this is not the case. My goal with this letter is not to upset you, but simply to let you in on my current thinking and take you where my research has taken me. I will say that I believe I am in the minority in my opinion. It is the above analysis that has led me to being more defensive in our portfolios.

You might be wondering just who I read and listen too. A few of those that shape my view are Jeremy Grantham, Janet Tavakoli, Robert Arnott, Bill Gross, Brian Wesbury, Jeremy Siegal, Robert Schiller, John Williams, James Grant, John Mauldin, John Hussman, Amity Shlaes, Nouriel Roubini, John Talbott and many, many others.

Given the depth of experts that I look too and read as often as they will write you might think that they’ve all come to an opinion, a consensus, you would be wrong. The experts I read have predictions that range from hyper-inflation to hyper-deflation and from a massive stock market boom to a massive stock market bust. Many of these experts lay out almost the same case, yet come to the exact opposite conclusion.

What is a person to do when the experts, some of who saw the last crash coming simply don’t agree or even have predictions that are diameterically opposed? The answer is you don’t bet on any one of them being right, you pursue several strategies that hedge against one another and attempt to build in enough flexibility that you can adapt and that is what we have done with your portfolios.

Risky versus Less Risky (used to be Non-Risky)

All of my client portfolio’s are made up of a mix of Risky and Less-Risky assets. I used to use the terms Risky and Non-Risky, but I’m not sure a “non-risky” asset exists. The portion of your portfolio that is placed into risky assets is dependent upon your need and ability to take risk in order to attempt to generate a higher return. Some of you will have no or little allocation to risky assets, others will have a substantial allocation.

Risky

The risky asset portion that I am recommending consists of three strategies:

Long-only Global Equity

Hedged Equity

Tactical Asset Allocation

The three strategies are designed to be more defensive in nature with the hope of capturing a reasonable return for the risk taken. These assets WILL fluctuate in value and sometimes wildly, however the hedged-equity and tactical portfolio’s are designed to fluctuate much less than the long-only portfolio.

The long-only portfolio is a simple buy-and-hold global stock index allocation. This portion of the portfolio will fluctuate the most. Given my above thoughts you may wonder why I include an allocation to stocks, the reasoning is that the stock market doesn’t obey me. Long-only stocks are a hedge against being wrong about the direction of the market and potentially a long-term hedge against inflation. Should we see another crash in stocks, you should expect to hear from me with the advice of increasing the assets in this strategy.

The hedged-equity strategy is managed by John Hussman (www.hussmanfunds.com) and he utilizes macro-economic analysis combined with valuation measures to determine how much of the risk of the market he would like to assume. When he believes there is more risk than potential return he will buy insurance (in the form of options) to hedge the portfolio against downside risk. When he believes stocks represent a good risk he will take those hedges off and potentially add some leverage. His prescient calls this decade have made his fund a steady performer, however it will underperform in major rallies. The price of underperformance during exuberant rallies is gladly paid for with a more limited downside. The goal is to outperform the market over a cycle with considerably less risk.

The final strategy is managed by Rob Arnott of Research Affiliates through PIMCO. Arnott believes that stocks are not priced to earn a reasonable premium and thus his fund is designed to find asset classes that offer a reasonable return for a given level of risk. This fund will fluctuate and can be invested in just about any type of asset class you can imagine depending on how the manager views the risk/return tradeoff. The goal is to provide a better return than the market with less risk, but more importantly to beat inflation by 5% annually.

The combination of these three strategies should reduce, not eliminate fluctuation in the portfolio which in the longer term can help your money compound quicker. In addition, the defensive nature will hopefully protect against market crashes. There is no assurance any of these strategies will work, however they have a demonstrated track record.

Less Risky

Less Risky means little to no fluctuation. For this portion of your portfolio my advice is to be short-term and high-quality. This means anything from FDIC insured savings accounts to highly rated and liquid fixed annuity products. Right now I believe flexibility is key and this means you want to keep your fixed income assets available to reinvest should inflation rear its head or interest rates rise. I do not believe now is the time to take on additional credit risk, though this may change. This strategy will hurt in the short-term as interest rates are terrible. You, the saver, are paying the price for the Wall Street bailouts, but at some point these rates must rise and being able to take advantage of this will be the reward of low short-term interest rates. If we end up with deflation you are well positioned, if we get inflation you are well positioned.

A portion of the fixed income or “less risky” part of your portfolio is invested in Treasury Inflation Protected Securities. While they have risen in value recently I don’t recommend selling, though their is potential for downside and I actually hope these securities fall in value as I’d like to own more, just at better prices than today.

So that is my strategy for your portfolio in general, each of you will have a slight variation due to the fact that I design portfolios to fit the individual. I hope that the changes we made will help in meeting your goals and I am available to speak or meet with you to discuss anything I’ve written more in depth.

Conclusion

I cannot say what 2010 will bring, it might be a boom, it might be a bust, what I can say is that I’ve done my best to position your portfolio according to my macro-economic outlook.

Scott

Margin of Safety, Hyperinflation, Deflation and Experts

The Lost Decade

As we start a new decade and leave behind a “lost one” (is it ironic that the TV show Lost became a hit this last decade?), many are wondering how they should position their money for the future. The answer as always is not so simple, but my purpose here is to provide a framework for how I have come to the decisions for my clients portfolios going forward.

A lot has happened in the past eighteen months, we’ve seen spectacular losses and spectacular gains. A lot has also changed, much of it for the worse, though you wouldn’t know it by the gains in the stock market. One thing that is clear is that the stock market continues to be a very volatile place to put one’s money and volatility is not your friend in retirement. While things appear to have returned to normal, all is not well and in my opinion their is more risk than potential return in the stock markets (generally).

Margin of Safety

Warren Buffet and Benjamin Graham preach(ed) that one should obtain a “margin of safety” when purchasing any asset. The reasoning being is that things can and do go wrong and if you include a cushion, you (or the asset) can survive. This concept is why home lenders used to require a down payment of 20 - 30% - if real estate prices became depressed the lender would still have a cushion to soften the blow in the event of a default. The same concept applies when you are driving a car, the faster you are driving the further distance you should keep from the vehicle in front of you in case that car does something unexpected. We’ve become a society of “margin-less asset purchasers” or MAP’s for short. We buy something regardless of price with the “hope” of selling to a greater fool should prices begin to fall, however at that point in time the greater fool doesn’t exist to sell to.

The Tens Aren’t the Eighties

Many have compared today’s market environment to the early 80’s and contend we are at the beginning of another great boom for stock prices, yet this thinking ignores many differences between then and now. Back in 1980 we had less than $1 Trillion in national debt (in terms of GDP less than half of today), almost exclusively held by Americans (in one form or another), a billion was a lot of money even back then. Today our national debt is approaching $13 trillion and will likely be $14 Trillion sometime in 2011. This does not include entitlement debt which has a present value north of $60 Trillion, nor does it include municipal or personal debt.

Back in the 80’s we began running deficits and we have never looked backed (no we did not ever have a balanced budget during the Clinton years, that was an accounting trick). We will never again be able to balance the budget, it is not possible and we may be stuck with a budget deficit of close to $2 Trillion annually for many, many years.

Back in 1980 the trailing ten-year average P/E Ratio (a measure of stock valuation, the lower the ratio the lower the value) on the stock market was about 8, today it is over 20 (close to where it was in October 2007, before the crash started). Back in the 80’s states and municipalities were not nearly as leveraged as they are today. Currently unemployment is running close to 22% according to ShadowStats.com. Housing is not fixed, in fact we are facing a foreclosure crisis worse than we faced just last year as an avalanche of option-ARM mortgage are set to adjust and as the four government programs set up to stop foreclosure have failed miserably. Banks are allowed to borrow at next to nothing from the Federal Reserve and invest in risk-free treasury bonds earning a nice spread while ignoring small business who need access to credit. The housing market is being propped up by the government in a manner never before witnessed in the United States, they have attacked on four fronts:

FHA continues to make loans with little or nothing down to people with less than perfect credit

The Congress passed a law that gives free money (up to $8000) to people who buy a home.

The Federal Reserve embarked on a program that doesn’t appear to be legal to print money to buy mortgage backed securities of Fannie and Freddie (government controlled mortgage agencies) in order to push down interest rates for borrowers and new home buyers.

Finally, accounting rules have been relaxed in order to allow mortgages to be carried on bank balance sheets at essentially whatever the banks want, thereby making insolvent institutions look solvent and delaying the purge in homes that are delinquent.

This never before attempted government intervention in housing has kept housing from falling further and even helped prices in certain areas, though new home sales have yet to recover and high-end homes are having severe issues. Fixing housing has not been a priority, pumping it back up has been the order of the day, but it won’t work. I contend that unless housing is fixed we won’t have a meaningful recovery. This doesn’t mean we won’t have a recovery or that stock prices won’t go ever higher. The coming resets in Option-ARM mortgages will peak once in 2010 and again in 2011, these peaks will rival the sub-prime mortgage peaks and if not dealt with properly will pose a major headwind for real-estate and all other things financial.

In my opinion there are several things that need to be done in order to fix our financial system.

First, we must reinstate some version of Glass-Steagal, the Great Depression era law that essentially separated investment banks from commercial banking.

Second, we must separate out the risk taking hedge-fund like trading from the investment banks. The investment banks have leveraged themselves up to the point that if they are wrong on their speculations they could bring down our entire financial system, yet we continue to allow them to exist with an implicit guarantee that we will bail them out if they get it wrong. This allows them to borrow at lower interest rates as investors believe they will be defended by the government in the event of a blowup. This hurts competition as the government essentially provides a subsidy to one set of financial institutions, those that get big enough.

Third, we must remove the doctrine of Too-Big-Too-Fail, allowing institutions that take on to much risk and get it wrong to fail. Taxpayers should not be on the hook for losses that should be taken by stock and bondholders. The TBTF doctrine has failed and its the taxpayers who are paying the price all while those who benefit (Wall Street) take home massive, record bonuses. This is not only morally reprehensible, it is bad economics.

Fourth, in implementing Too-Big-Too-Fail we must breakup many of the large banks (Citibank, BofA, etc) and reduce the amount of FDIC insurance that is provided. Smaller institutions provide more competition and if regulated properly will not be able to take on the leverage and poorly underwritten assets that the large banks have purchased.

Fifth, we must reign in the Federal Reserve. The Fed has done more to devalue our currency than most understand. Since the creation of the Fed the dollar has fallen over 95% in value. While the Fed has been credited with saving the economy (Bernanke was named Time Man of the Year), it is more likely he has simply delayed the inevitable and made things much worse.

Sixth, we must fix housing. There are several solutions, some that include taxpayer money, others that don’t. We should make economically sound financial decisions like offering Principal Reductions when it makes sense to do so. John Hussman of the Hussman Funds has also come up with a system to deal rationally with this problem. This is essential.

Seventh, we must fix our entitlement problem (medicare, medicaid, social security). Our total national debt including entitlements is nearing $120 Trillion, of this over $100 Trillion is the present value of the short fall in Social Security and Medicare (Part D included). Did you know that Medicare Part D, which was just passed into law a few years ago under the Bush Administration already has a present value deficit greater than that of Social Security?

Eighth, we need to regulate Credit Default Swaps and make the system more transparent.

Implementing the above fixes will be politically difficult given the enormous amount of money that finances the campaigns of our politicians, but without these reforms and others we are destined to be on a boom-bust cycle for decades or be thrust into a greater depression than we are in currently. In addition, it is many of the current politicians that have created much of the chaos by passing budgets that are unsustainable. This is not unique to one-party. Perhaps throwing the bums out and starting over should be number one on my list above.

Experts

At this point you are probably wishing you hadn’t read this commentary, you might think I’m overly pessimistic and that perhaps I’ve thrown in with the crazies. I assure you this is not the case. My goal with this letter is not to upset you, but simply to let you in on my current thinking and take you where my research has taken me. I will say that I believe I am in the minority in my opinion. It is the above analysis that has led me to being more defensive in our portfolios.

You might be wondering just who I read and listen too. A few of those that shape my view are Jeremy Grantham, Janet Tavakoli, Robert Arnott, Bill Gross, Brian Wesbury, Jeremy Siegal, Robert Schiller, John Williams, James Grant, John Mauldin, John Hussman, Amity Shlaes, Nouriel Roubini, John Talbott and many, many others.

Given the depth of experts that I look too and read as often as they will write you might think that they’ve all come to an opinion, a consensus, you would be wrong. The experts I read have predictions that range from hyper-inflation to hyper-deflation and from a massive stock market boom to a massive stock market bust. Many of these experts lay out almost the same case, yet come to the exact opposite conclusion.

What is a person to do when the experts, some of who saw the last crash coming simply don’t agree or even have predictions that are diameterically opposed? The answer is you don’t bet on any one of them being right, you pursue several strategies that hedge against one another and attempt to build in enough flexibility that you can adapt and that is what we have done with your portfolios.

Risky versus Less Risky (used to be Non-Risky)

All of my client portfolio’s are made up of a mix of Risky and Less-Risky assets. I used to use the terms Risky and Non-Risky, but I’m not sure a “non-risky” asset exists. The portion of your portfolio that is placed into risky assets is dependent upon your need and ability to take risk in order to attempt to generate a higher return. Some of you will have no or little allocation to risky assets, others will have a substantial allocation.

Risky

The risky asset portion that I am recommending consists of three strategies:

Long-only Global Equity

Hedged Equity

Tactical Asset Allocation

The three strategies are designed to be more defensive in nature with the hope of capturing a reasonable return for the risk taken. These assets WILL fluctuate in value and sometimes wildly, however the hedged-equity and tactical portfolio’s are designed to fluctuate much less than the long-only portfolio.

The long-only portfolio is a simple buy-and-hold global stock index allocation. This portion of the portfolio will fluctuate the most. Given my above thoughts you may wonder why I include an allocation to stocks, the reasoning is that the stock market doesn’t obey me. Long-only stocks are a hedge against being wrong about the direction of the market and potentially a long-term hedge against inflation. Should we see another crash in stocks, you should expect to hear from me with the advice of increasing the assets in this strategy.

The hedged-equity strategy is managed by John Hussman (www.hussmanfunds.com) and he utilizes macro-economic analysis combined with valuation measures to determine how much of the risk of the market he would like to assume. When he believes there is more risk than potential return he will buy insurance (in the form of options) to hedge the portfolio against downside risk. When he believes stocks represent a good risk he will take those hedges off and potentially add some leverage. His prescient calls this decade have made his fund a steady performer, however it will underperform in major rallies. The price of underperformance during exuberant rallies is gladly paid for with a more limited downside. The goal is to outperform the market over a cycle with considerably less risk.

The final strategy is managed by Rob Arnott of Research Affiliates through PIMCO. Arnott believes that stocks are not priced to earn a reasonable premium and thus his fund is designed to find asset classes that offer a reasonable return for a given level of risk. This fund will fluctuate and can be invested in just about any type of asset class you can imagine depending on how the manager views the risk/return tradeoff. The goal is to provide a better return than the market with less risk, but more importantly to beat inflation by 5% annually.

The combination of these three strategies should reduce, not eliminate fluctuation in the portfolio which in the longer term can help your money compound quicker. In addition, the defensive nature will hopefully protect against market crashes. There is no assurance any of these strategies will work, however they have a demonstrated track record.

Less Risky

Less Risky means little to no fluctuation. For this portion of your portfolio my advice is to be short-term and high-quality. This means anything from FDIC insured savings accounts to highly rated and liquid fixed annuity products. Right now I believe flexibility is key and this means you want to keep your fixed income assets available to reinvest should inflation rear its head or interest rates rise. I do not believe now is the time to take on additional credit risk, though this may change. This strategy will hurt in the short-term as interest rates are terrible. You, the saver, are paying the price for the Wall Street bailouts, but at some point these rates must rise and being able to take advantage of this will be the reward of low short-term interest rates. If we end up with deflation you are well positioned, if we get inflation you are well positioned.

A portion of the fixed income or “less risky” part of your portfolio is invested in Treasury Inflation Protected Securities. While they have risen in value recently I don’t recommend selling, though their is potential for downside and I actually hope these securities fall in value as I’d like to own more, just at better prices than today.

So that is my strategy for your portfolio in general, each of you will have a slight variation due to the fact that I design portfolios to fit the individual. I hope that the changes we made will help in meeting your goals and I am available to speak or meet with you to discuss anything I’ve written more in depth.

Conclusion

I cannot say what 2010 will bring, it might be a boom, it might be a bust, what I can say is that I’ve done my best to position your portfolio according to my macro-economic outlook.

Bernanke On The Way Out?

Stay tuned, Fed Chairman Ben Bernanke may not have the votes necessary to hold onto his job - could this lead to a possible resignation? This is good news, but this will lead to additional volatility.

Scott Dauenhauer

Scott Dauenhauer

Thursday, January 21, 2010

Scandal: Albert Edwards Alleges Central Banks Were Complicit In Robbing The Middle Classes

Very interesting piece on the real issue this country faces - The Federal Reserve.

Scott Dauenhauer CFP, MSFP, AIF

Scott Dauenhauer CFP, MSFP, AIF

FDIC Chief Got Bank of America Loans While Working On Its Rescue

I like much of what Sheila Bair has done and many of her ideas, but what appears to have happened here was a severe lapse of judgement if the facts prove true. The way Bair went about getting this loan doesn't feel right and she knew better (given what happened to Dodd). Why didn't she start the process out by bringing in the attorney's instead of getting a retroactive waiver?

This is going to hurt her reform efforts and jeopardize any chance she had of advancement, unless of course the administration continues to award based on ethical lapses (can somebody say Geithner?). Perhaps this is the perfect opportunity to have a clean sweep, a Trifecta if you will - get rid of Bernanke, Geithner and Bair at the same time and bring in people who have the credentials to get things done - and no, I'm not talking about a bringing in a bunch of ex-Goldman execs.

Scott Dauenhauer CFP, MSFP, AIF

Obama/Volcker - Return of Glass-Steagall?

President Obama today is set to announce reforms aimed at curbing the size of our nation's banks and the risks they are allowed to take. It appears that Paul Volcker is beginning to have the influence many of us hoped for on the Obama administration. The details are sparse at this point, though it appears to fall short of nixing the Too Big Too Fail doctrine that has permeated the Republican and Democrat parties these past few decades.

While this appears to be a good first step it is unclear what the new regs will be, how they will be applied and whether the financial industry will be able to defeat them. Its too early to tell.

The good news is that we are finally starting to see a move in the right direction (I think, remember, there aren't many details yet). The existence of Too Big Too Fail is a huge moral hazard to our economy and must be dealt with, this might not be the preferred way and at the end of the day I may oppose, but for the first time in this financial crisis their might be the signs of a ray of hope emerging.

On a separate note, for those who care, I don't support the "bank fee" that the administration wants to levy on bank liabilities. Its not that I have any love for Wall Street, I just don't see the merit in it. The fee will end up being paid by consumers and it punishes in the wrong way some of those that helped cause the financial crisis while ignoring the government responsibility in the crisis.

Scott Dauenhauer CFP, MSFP, AIF

While this appears to be a good first step it is unclear what the new regs will be, how they will be applied and whether the financial industry will be able to defeat them. Its too early to tell.

The good news is that we are finally starting to see a move in the right direction (I think, remember, there aren't many details yet). The existence of Too Big Too Fail is a huge moral hazard to our economy and must be dealt with, this might not be the preferred way and at the end of the day I may oppose, but for the first time in this financial crisis their might be the signs of a ray of hope emerging.

On a separate note, for those who care, I don't support the "bank fee" that the administration wants to levy on bank liabilities. Its not that I have any love for Wall Street, I just don't see the merit in it. The fee will end up being paid by consumers and it punishes in the wrong way some of those that helped cause the financial crisis while ignoring the government responsibility in the crisis.

Scott Dauenhauer CFP, MSFP, AIF

Monday, January 18, 2010

Risk, The Banks and Stimulus

If lowering interest rates to zero to induce citizens to take risk (any risk) with their money is good and needed, why is it that the banks need not follow the same directive? Why is it okay for citizens to earn nothing on their money or be forced to take more risk to earn slightly more than nothing and yet the banks get to borrow at nothing interest rates and use the proceeds to buy risk-free treasuries with a higher yield? Isn't the idea to get money flowing again?

Banks are not lending, even to credit worthy consumers. I was recently declined for a fully collateralized auto loan due to the year my house was purchased...what? The banks are inventing reasons to decline people. If this is recovery I'd hate to see what a recession looks like.

In re-memberance of that mighty $800 billion stimulus that failed to contain unemployment, alas it is risen from the dead and is about to inflict its wrath on our nation. In 2009, less than $300 billion of the stimulus was spent, leaving nearly $500 billion ready to prime the economy in 2010, an election year nonetheless (no coincidence). This will help in the short term (and if it doesn't then we are really in trouble), but detract in the long term. It seems everyone is bullish again, maybe a good time to be bearish?

The banks are not lending because their balance sheets are highly impaired, this won't change anytime soon. We have not dealt with any of the problems that caused this depression, nor does it appear we are likely too. On to the next boom...and bust.

Scott Dauenhauer

Banks are not lending, even to credit worthy consumers. I was recently declined for a fully collateralized auto loan due to the year my house was purchased...what? The banks are inventing reasons to decline people. If this is recovery I'd hate to see what a recession looks like.

In re-memberance of that mighty $800 billion stimulus that failed to contain unemployment, alas it is risen from the dead and is about to inflict its wrath on our nation. In 2009, less than $300 billion of the stimulus was spent, leaving nearly $500 billion ready to prime the economy in 2010, an election year nonetheless (no coincidence). This will help in the short term (and if it doesn't then we are really in trouble), but detract in the long term. It seems everyone is bullish again, maybe a good time to be bearish?

The banks are not lending because their balance sheets are highly impaired, this won't change anytime soon. We have not dealt with any of the problems that caused this depression, nor does it appear we are likely too. On to the next boom...and bust.

Scott Dauenhauer

Friday, January 15, 2010

Big Picture: Record Bank Bonuses Based On Record Bank Fraud

Barry Ritholz gets it right with this short opinion piece on bank bonuses.

Scott Dauenhauer CFP, MSFP, AIF

Ask yourself how hard it is for any finance firm to make money — risk free! — when they can borrow from the Federal Reserve at a rate of zero, and then turnaround and “lend” that same cash to the Treasury (buying bonds) at 3% ?

Scott Dauenhauer CFP, MSFP, AIF

From The Deflation Camp

I've linked above to a newsletter put out by Hoisington Management and it argues that we are in for deflation, not inflation and the long term interest rates will fall, not increase. It is a well written piece and you should pay attention. Right now there is a battle going on (as I've chronicled) between the Inflationists and the Deflationists, both may turn out to be right. I'm not in either camp, the reason I haven't joined one side or the other is that I think both sides have done a good job of making their case and I'm torn. I've chosen to set up my clients portfolio's with enough flexibility to benefit either way, but not in a major or speculative way. I believe we could have deflation followed by a great inflation. This is not to discount the possibility that we will simply enter into an inflationary period. Five years from now the answer will have seemed obvious, today, not so much.

Scott Dauenhauer CFP, MSFP, AIF

Scott Dauenhauer CFP, MSFP, AIF

Thursday, January 14, 2010

Humor Break: Jon Stewart Takes On Wall Street Bonuses

| The Daily Show With Jon Stewart | Mon - Thurs 11p / 10c | |||

| Clusterf#@k to the Poor House - Wall Street Bonuses | ||||

| ||||

Wednesday, January 13, 2010

WSJ: BofA REIT Dealings

In what was supposed to be a puff piece on Bank of America taking over the IPO market for Real Estate Investment Trusts it seems the Wall Street Journal may have exposed a practice that could come back to haunt that bank, and taxpayers. It appears that BofA is dangling the carrot of big credit line facilities for hurting REIT's in order to win investment banking business (stock issuance). The following quote from the story seems to confirm this:

BofA earns big fees on these stock issuance deals, but what about the risk they are taking by extending the credit and using the credit as a way to attract the stock underwriting business? While this might not be anything new we should be concerned because commercial real estate isn't exactly in a good position right now and if the downturn is extended we could see BofA become an owner of yet more illiquid real estate......requiring further bailouts.

Scott Dauenhauer CFP, MSFP, AIF

"ProLogis Chief Financial Officer Bill Sullivan said the company tapped Bank of America to run the stock offering because of the lending relationship.

"Our view, very consciously, was, 'Hey, let's let these guys make some money … and that will help us as we go to deal with some of the bank-line issues,'" Mr. Sullivan said."

BofA earns big fees on these stock issuance deals, but what about the risk they are taking by extending the credit and using the credit as a way to attract the stock underwriting business? While this might not be anything new we should be concerned because commercial real estate isn't exactly in a good position right now and if the downturn is extended we could see BofA become an owner of yet more illiquid real estate......requiring further bailouts.

Scott Dauenhauer CFP, MSFP, AIF

Tuesday, January 12, 2010

Humor Break: Colbert: Move Your Money

| The Colbert Report | Mon - Thurs 11:30pm / 10:30c | |||

| Move Your Money - Eugene Jarecki | ||||

| ||||

Monday, January 11, 2010

America slides deeper into depression as Wall Street revels

"But it also masks the continued rot in the housing market, allows lenders to hide losses, and stores up an ever larger overhang of unsold properties. It takes heroic naivety to think the US housing market has turned the corner (apologies to Goldman Sachs, as always). The fuse has yet to detonate on the next mortgage bomb, $134bn (£83bn) of "option ARM" contracts due to reset violently upwards this year and next.

US house prices have eked out five months of gains on the Case-Shiller index, but momentum stalled in October in half the cities even before the latest surge of 40 basis points in mortgage rates. Karl Case (of the index) says prices may sink another 15pc. "If the 2008 and 2009 loans go bad, then we're back where we were before – in a nightmare."

This gloom and doom article should not be dismissed or discounted.

Scott Dauenhauer CFP, MSFP, AIF

The Venezuelan Devaluation & What It Means To You

There isn't much talk about it, but our fine neighbor down in Venezuela has decided that a devaluation is in order. The currency is being devalued by 50%. This doesn't mean much to most Americans and it is interesting that it is not getting much play in the U.S. media. With the announcement came threats from Chavez that he would use the National Guard to seize ANY business that raised prices domestically.

While I did teach International Finance for one semester at University I must acknowledge that I have much too learn. But I think I can demonstrate in short order for you why prices would rise in a devaluation.

First, the devaluation in this instance means that "stuff" imported into Venezuela will now cost twice as much. That bottle of wine from Napa Valley that cost 20 Bolivar would now cost 40 Bolivar to the consumer. Now, if there were domestic producers of wine in Venezuela (I don't know if there is) the competition they had before the devaluation has been obliterated. They no longer have to compete with foreign imported wine and thus could raise their price. If they just raised their price to 30 Bolivar per bottle (keep in mind I have no idea how many Bolivar it takes to buy a bottle of wine, this is for demonstration purposes only) they would still be 25% cheaper (or the foreign wine would b 33% more expensive) than their foreign competitor, yet they would receive an extra 50% in revenue and could see big profit. Eventually what would happen is prices would rise, thus inflation. But of course Chavez has this all under control as he will seize your business if you decide to raise prices (even if you weren't making any money at the previous price).

The devaluation is supposed to make Venezuelans exports cheaper, which it will in the short term - the hope is that the domestic economy will pick up and have stronger demand from the outside world. The problem is that with stronger demand you usually in the short term get inputs that are more costly as well....which forces you to raise prices, which is illegal. Perhaps they'll be allowed to sell products to other countries at higher prices, just not to their own people.

Any way you look at Venezuela it is clear that this country is on a crash course for anarchy, social unrest, revolution and mass murder. These are not the inevitable outcomes of devaluation, our currency will eventually continue its downward devaluation trajectory (which is not good), but hopefully without the bloodshed.

My main point was really that a devaluation doesn't solve long term problems, it simply is a short-term band-aid.

Scott Dauenhauer CFP, MSFP, AIF

While I did teach International Finance for one semester at University I must acknowledge that I have much too learn. But I think I can demonstrate in short order for you why prices would rise in a devaluation.

First, the devaluation in this instance means that "stuff" imported into Venezuela will now cost twice as much. That bottle of wine from Napa Valley that cost 20 Bolivar would now cost 40 Bolivar to the consumer. Now, if there were domestic producers of wine in Venezuela (I don't know if there is) the competition they had before the devaluation has been obliterated. They no longer have to compete with foreign imported wine and thus could raise their price. If they just raised their price to 30 Bolivar per bottle (keep in mind I have no idea how many Bolivar it takes to buy a bottle of wine, this is for demonstration purposes only) they would still be 25% cheaper (or the foreign wine would b 33% more expensive) than their foreign competitor, yet they would receive an extra 50% in revenue and could see big profit. Eventually what would happen is prices would rise, thus inflation. But of course Chavez has this all under control as he will seize your business if you decide to raise prices (even if you weren't making any money at the previous price).

The devaluation is supposed to make Venezuelans exports cheaper, which it will in the short term - the hope is that the domestic economy will pick up and have stronger demand from the outside world. The problem is that with stronger demand you usually in the short term get inputs that are more costly as well....which forces you to raise prices, which is illegal. Perhaps they'll be allowed to sell products to other countries at higher prices, just not to their own people.

Any way you look at Venezuela it is clear that this country is on a crash course for anarchy, social unrest, revolution and mass murder. These are not the inevitable outcomes of devaluation, our currency will eventually continue its downward devaluation trajectory (which is not good), but hopefully without the bloodshed.

My main point was really that a devaluation doesn't solve long term problems, it simply is a short-term band-aid.

Scott Dauenhauer CFP, MSFP, AIF

The Economist: Bubble Warning

Not everyone thinks this recovery is real and this article demonstrates the thinking as to why. Its not a long article, but it will give you a good idea of what has been created that worries so many people, myself included.

2010 may very well be a boom year, with the stimulus spending finally hitting in full force and stocks showing better earnings, but this masks the true condition of our financial system and our government debt. The one major characteristic of bubbles is that you don't know when they will end, they can persist for a long time.

Scott Dauenhauer CFP, MSFP, AIF

Quoted Again in Wall Street Journal "Refresh Your Retirement Plan"

Not a bad way to start out the year (despite my Oregon Ducks losing in the Rose Bowl), I was quoted in the Wall Street Journal again in an article by Tom Lauricella.

Scott Dauenhauer CFP, MSFP, AIF

Scott Dauenhauer CFP, MSFP, AIF

Subscribe to:

Posts (Atom)