Great article by Tara Siegel Bernard on target-date funds. I'm quoted as well. I think the last sentence sums it up best, its how much you put into your retirement plan that matters the most.

Scott Dauenhauer CFP, MSFP, AIF

949-916-6238

www.meridianwealth.com

Monday, June 29, 2009

Monday, June 22, 2009

No Recovery Without Failure

I'll expand more on this concept later, but the irony of our financial problems today lay partially in the failure to allow failure. Without failure there can be no success, this is the essence of creative destruction. Our system of bailouts has distorted the marketplace and rewarded failure while punishing success. What about those that lost money buying the stocks of bailed out financial firms you may ask? That is punishment, however please explain to me why taxpayers had to step in ahead of the bond holders of these companies? Please tell me why my hard earned money, which was not invested in bank stocks was required to bailout bond holders of these firms when they in fact made an active choice to invest in these firms? Shouldn't people who make an active decision to bear investment risk actually take losses before the taxpayers are expected too? This failure to allow bond holders to lose money will have severe repercussions long term throughout our entire capital system.

By not allowing failure we prop up companies like Citigroup and GM we punish the companies that could have gained market-share as a a result of the failure. This is how markets work, good decisions are rewarded (eventually) and bad punished (or so we thought). Instead we have created a system where the good decisions are no longer being rewarded (at least like they should) and the bad decisions are in fact being rewarded (bailed out bond holders and government backing). This market distortion can only continue for so long - at some point it must fail. The problem with this new system failing is that it will be much, much worse than had we allowed failure to happen in the first place.

Scott Dauenhauer CFP, MSFP, AIF

By not allowing failure we prop up companies like Citigroup and GM we punish the companies that could have gained market-share as a a result of the failure. This is how markets work, good decisions are rewarded (eventually) and bad punished (or so we thought). Instead we have created a system where the good decisions are no longer being rewarded (at least like they should) and the bad decisions are in fact being rewarded (bailed out bond holders and government backing). This market distortion can only continue for so long - at some point it must fail. The problem with this new system failing is that it will be much, much worse than had we allowed failure to happen in the first place.

Scott Dauenhauer CFP, MSFP, AIF

Monday, June 15, 2009

NY Times: Building a Cushion Into Investments for When Inflation Returns

I really like Tara Siegel Bernard, she is an interesting personal finance writer. Today I got mentioned in this New York Times article that basically speaks to inflation. For the record, this is the first time in the New York Times which pretty much means I've hit every major publication in the U.S. You name it, I've probably been quoted.

Anyway, if you've got a few, hit the link above.

Scott Dauenhauer CFP, MSFP, AIF

www.meridianwealth.com

Anyway, if you've got a few, hit the link above.

Scott Dauenhauer CFP, MSFP, AIF

www.meridianwealth.com

Hussman: The Outlook is Not Up, But Very Widely Sideways

Another great update by John Hussman, Ph.D.

Scott Dauenhauer CFP, MSFP, AIF

Scott Dauenhauer CFP, MSFP, AIF

Thursday, June 11, 2009

WSJ: Are Inflation Fears Over-inflated?

Here is a quick video run down of what could potentially cause inflation.

embed src="http://s.wsj.net/media/swf/main.swf" bgcolor="#FFFFFF" flashVars="videoGUID={77928487-864C-4BB4-BDBB-1DDC191C7554}&playerid=1000&plyMediaEnabled=1&configURL=http://wsj.vo.llnwd.net/o28/players/&autoStart=false” base="rtmpt://wsj.fcod.llnwd.net/a1318/o28/video" name="main" width="512" height="363" seamlesstabbing="false" type="application/x-shockwave-flash" swLiveConnect="true" pluginspage="http://www.macromedia.com/shockwave/download/index.cgi?P1_Prod_Version=ShockwaveFlash">

Scott Dauenhauer CFP, MSFP, AIF

www.meridianwealth.com

embed src="http://s.wsj.net/media/swf/main.swf" bgcolor="#FFFFFF" flashVars="videoGUID={77928487-864C-4BB4-BDBB-1DDC191C7554}&playerid=1000&plyMediaEnabled=1&configURL=http://wsj.vo.llnwd.net/o28/players/&autoStart=false” base="rtmpt://wsj.fcod.llnwd.net/a1318/o28/video" name="main" width="512" height="363" seamlesstabbing="false" type="application/x-shockwave-flash" swLiveConnect="true" pluginspage="http://www.macromedia.com/shockwave/download/index.cgi?P1_Prod_Version=ShockwaveFlash">

Scott Dauenhauer CFP, MSFP, AIF

www.meridianwealth.com

Wednesday, June 10, 2009

A New Mark-to-Market World - Banks Lie

In today's Wall Street Journal an interesting article was written that focuses on individuals and corporations who are trying to make a buck by buying bad "toxic" mortgages and then working them out, pocketing some money in the meantime. The problem? They can't find any "toxic" mortgages to buy, at least not at prices they are willing to pay. A passage from the article:

"Initially, we thought there would be a plethora of opportunities" to buy loans, says Mr. DellaCamera, 55 years old, who headed trading at hedge fund Elliott Associates for more than a decade. "But we pulled back from buying these loans because the pricing isn't there and we were having trouble hedging." He calls servicing troubled loans a "tremendous opportunity."

Because most mortgage-loan sales are private, statistics are difficult to come by. Prices currently vary from 20 cents per dollar of unpaid principal for some of the riskiest subprime mortgages to nearly 90 cents on the dollar for current loans to borrowers in strong housing markets, says Kingsley Greenland, chief executive of DebtX, an online marketplace for loans.

Those types of prices would produce losses far greater than most have reserved for, says Keefe, Bruyette & Woods analyst Frederick Cannon. "Banks are essentially holding loans in the system at a value of 97.5 cents on the dollar," he says.

Did you get that? Banks are holding loans "at a value of 97.5 cents on the dollar." Can somebody please explain this too me?

This is the result of the change to Mark-to-Market rules which allow the banks to carry worthless or highly suspect loans on their balance sheets at prices that have no relation to economic value. I think that Mark-to-Market was ripe to be changed, however a return to Mark-to-Fantasy has begun.

Do you ever wonder why just a few months ago the banking system was on the brink of insolvency and all the talk was about nationalization.......and now everything is fine and banks are paying back TARP? I believe the answer lies in the loosening of mark-to-market rules and the fact that banks are carrying loans at near full value when in fact the collateral securing those loans are severely impaired and no improvement is expected. The stress-tests were a joke and the banks are not as clean as we are being led to believe. This should scare you, it scares me.

Scott Dauenhauer CFP, MSFP, AIF

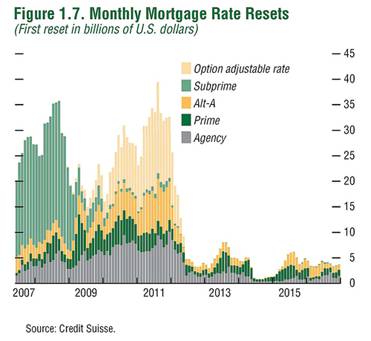

Hussman: Context Matters

Hussman takes us through how he determines his hedges. In addition, he points out the huge increase in potential foreclosures coming our way. I've attached a graph, it ain't pretty.

Scott Dauenhauer CFP, MSFP, AIF

www.meridianwealth.com

949-916-6238

Monday, June 08, 2009

Deflation or Inflation? Or Both?

The big debate right now with economists is whether the United States will experience Inflation or Deflation. The short term view seems to be that deflation is a possibility, though the long view is that inflation is more likely. However, there are bright economists on both sides of the debate - both however cannot be right.

The inflation view, which I favor basically argues that massive deficits will lead to inflation. While deficits in and of themselves don't lead to inflation, these deficits are deemed to be so large (on top of already massive spending programs) that instead of financing the deficits with existing money supply, the Federal Reserve will have to finance them by purchasing the debt the treasury issues - thus expanding the money supply greatly and diluting the value of the dollar.

The deflation view makes sense in the short term as unemployment rises and people have less to spend, the prices of goods fall.

I'm not sure its wise to make a bet either way, but to maintain flexibility to react to whichever comes our way. My bigger fear is inflation and the high interest rates that could come with it.

Scott Dauenhauer CFP, MSFP, AIF

www.meridianwealth.com

Tuesday, June 02, 2009

Vintage pro-inflation propaganda

This is not a humor break, its the government in the 30's attempting to convince everyone that Inflation is great and will solve all your problems. Why is this important? I'm about to post two articles by individuals that tell you why.

Scott Dauenhauer CFP, MSFP, AIF

www.meridianwealth.com

Hussman: Anything But Academic

No commentary needed from me, just read it. Turns out Hussman was a student of John Taylor (prior post).

Scott Dauenhauer CFP, MSFP, AIF

www.meridianwealth.com

Scott Dauenhauer CFP, MSFP, AIF

www.meridianwealth.com

Exploding Debt Threatens America

Excerpt of article below by John Taylor

“A government debt burden of that [100 per cent] level, if sustained, would in Standard & Poor’s view be incompatible with a triple A rating,” as the risk rating agency stated last week.

I believe the risk posed by this debt is systemic and could do more damage to the economy than the recent financial crisis. To understand the size of the risk, take a look at the numbers that Standard and Poor’s considers. The deficit in 2019 is expected by the CBO to be $1,200bn (€859bn, £754bn). Income tax revenues are expected to be about $2,000bn that year, so a permanent 60 per cent across-the-board tax increase would be required to balance the budget. Clearly this will not and should not happen. So how else can debt service payments be brought down as a share of GDP?

Inflation will do it. But how much? To bring the debt-to-GDP ratio down to the same level as at the end of 2008 would take a doubling of prices. That 100 per cent increase would make nominal GDP twice as high and thus cut the debt-to-GDP ratio in half, back to 41 from 82 per cent. A 100 per cent increase in the price level means about 10 per cent inflation for 10 years. But it would not be that smooth – probably more like the great inflation of the late 1960s and 1970s with boom followed by bust and recession every three or four years, and a successively higher inflation rate after each recession."

I encourage you to read this article. Inflation is not an immediate threat, however given that a 60% tax rate is not something that could be passed by any congress (lets hope this to be true) the only way out is inflation (short of reigning in government spending, what a concept).

Scott Dauenhauer CFP, MSFP, AIF

www.meridianwealth.com

949-916-6238

Subscribe to:

Posts (Atom)