In December of 2008 I wrote the following post "Opinion: Seniors Victimized By Low Rates":

"With the Feds lowering short term rates to zero and attempting to lower long term rates by buying Treasury bonds homeowners with equity and good credit are doing handstands. Perhaps all of this maneuvering will help, perhaps not, only time will tell. What is left out of the story however are those who are effectively subsidizing this policy - Seniors who rely on reasonable interest rates for income.

While the meltdown in the stock market has been epic, at one point a tad over 50%. The meltdown of interest rates has been complete. Last year a senior could get a rate of 5 - 6% on their money with little, even no risk in most places. I even have a few clients who locked in a risk free rate of 7% for five years in a 457 plan they had access to. For seniors who were earning 5%, they would get about $5,000 per $100,000 invested. Today that rate is now nearly zero. You can shop around and get 2 or 3% in a CD, though you may even have to go out five years to do that. That would be around $2,000 per year of income for every $100,000 invested a drop of 60%.

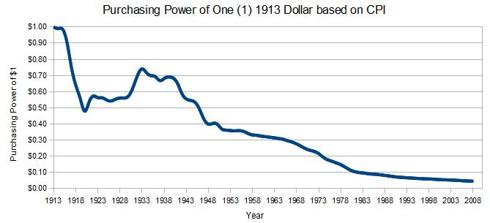

What is worse is that the inflationary forces that have appeared to disappear and even reverse into deflation (which does actually make the $2,000 go farther......until you factor in that seniors are not experiencing deflation) are short term. The return of inflation is inevitable. This will further decimate the savings, though it will probably raise rates.

These low interest rates will push seniors to look for higher rates, not thinking about the higher risks. They will be marketed to by weasels who will attempt to lure them into their faux products promising higher returns with little or no risk - a combination that doesn't exist (can you say Madoff).

Be vigilant out there and stay on your guard."

14 months later Charles Schwab has basically written the same thing in a Wall Street Journal opinion piece. While I wholeheartedly agree with him I wonder where he was in December of 2008? I'm seeing people falling into the trap set by eager scamsters who lure seniors and retirees in with high guaranteed rates that are really just products that enrich the person selling or outright Ponzi schemes (okay, I'll admit, Bernanke and Co. are doing a pretty good job of running their own Ponzi - but they can legally print money).

I just have to wonder where Chuck was back then and quite honestly where the hell the rest of these so called leaders have been? Oh, that's right, getting bailed out (note: Schwab was not a recipient of bailout funds).

Bernanke is either wrong or lying. He says the economy is recovering, but it can withstand even a 1% interest rate hike - that is pure and utter B.S. OR, the economy is not recovering and he is lying to us. There are no other options.

For those seniors out there who are struggling, I feel for you, its time to get back what is rightfully yours - a reasonable and safe rate of return on your money.

Scott Dauenhauer CFP, MSFP, AIF