For almost two years now I've stated that the U.S. is in a depression. I've been clear that I don't believe we are in a depression that is as big as the Great Depression was (though have never discounted the possibility). I've taken issue with the term "Great Recession" because it ignores history and tries to spin our actual economic situation. The term depression has not been used since the Great Depression, but was a common term before it. My point is that the evidence is clear we aren't in a garden variety recession, its a depression - but its not the end of the world. It seems that most economists and talking heads believe the term depression can only be used if you are talking about the end of society (ok, perhaps now I'm engaging in a bit of hyperbole, but not much).

Over at the Naked Capitalist blog (www.nakedcapitalist.com) Yves Smith has linked to a Washington Post blog which attempts to compare today's economy to that of the Great Depression. The comparison will likely change your mind as to how this economic environment should be termed, at the very least we should refer to it as a "Depression". Maybe "Silent Depression" should be the moniker.

Hit the topic above for the jump. I've also embedded two of the referenced videos.

Scott Dauenhauer, CFP, MSFP, AIF

Wednesday, December 29, 2010

Monday, December 27, 2010

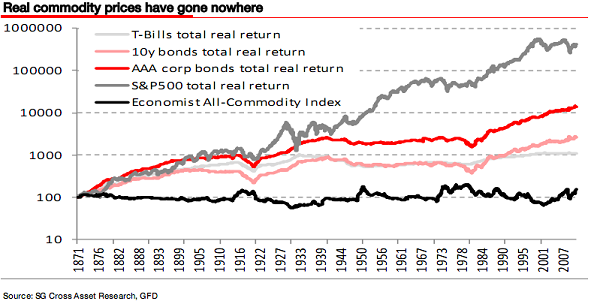

PragCap: COMMODITIES & THE 130+ YEAR BEAR MARKET

The Pragmatic Capitalist (www.pragcap.com) is one of my favorite blogs - even if we don't always agree. Mr. Roche has posted an excellent piece on Commodities which pretty much represents my thinking on the topic (perhaps ex-oil). I encourage you to read the entire piece, it is well worth it and provides an entirely different perspective than Glenn Beck's advertisers.

A few of my favorite portions:

Benjamin Graham Quote:

“An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.” - Benjamin Graham

Seth Klarman Quote:

“Buying anything that is a collectible, has no cash flow, and is based only on a future sale to a greater fool, if you will—even if that purchaser is not a fool—is speculating. The “investment” might work—owing to a limited supply of Monets, for example—but a commodity doesn’t have the same characteristics as a security, characteristics that allow for analysis. Other than a recent sale or appreciation due to inflation, analyzing the current or future worth of a commodity is nearly impossible.

The line I draw in the sand is that if an asset has cash flow or the likelihood of cash flow in the near term and is not purely dependent on what a future buyer might pay, then it’s an investment. If an asset’s value is totally dependent on the amount a future buyer might pay, then its purchase is speculation. The hardest commodity-like asset to categorize is land, an asset that is valuable to a future buyer because it will deliver cash flow, not because it will be sold to a future speculator.”

From Roche and Klarman:

There’s an interesting counterargument that can be made for a commodity such as gold, however. Doesn’t its currency like characteristics make it unique? Seth Klarman says no:

“Gold is unique because it has the age-old aspect of being viewed as a store of value. Nevertheless, it’s still a commodity and has no tangible value, and so I would say that gold is a speculation. But because of my fear about the potential debasing of paper money and about paper money not being a store of value, I want some exposure to gold.”

Hope you enjoy - you will also find the comment section provides even more learning opportunities.

Scott Dauenhauer CFP, MSFP, AIF

Wednesday, December 15, 2010

MISH: Chanos on China Bubble

China seems to be all anyone can talk about these days, is its centrally planned economy the wave of the future as some would like you to believe? My answer is no, the Soviet Union demonstrated that while a centrally planned economy can survive for a long time, it will never allocate resources correctly. Jim Chanos appeared on CNBC with a stunning outlook on China.

Humor Break: Colbert vs. Goldman Sachs

| The Colbert Report | Mon - Thurs 11:30pm / 10:30c | |||

| Goldman Sachs Lawyers Want Buckley T. Ratchford's Card Back | ||||

| ||||

Monday, December 06, 2010

Big Ben Explains Things

A few things that concern me:

Bernanke says that QE is not inflationary, but that he is worried about deflation and won't let it happen....if QE is not inflationary then how can it fight deflation?

I don't believe QE is inflationary, its an asset swap (as Bernanke states). This doesn't mean that others won't believe it is inflationary and push up asset prices as a speculation.

I think the worst quote is when the interviewer asks whether he is able to control things and he said he was "100% confident". Famous last words.

He says the goal is to lower rates, yet doesn't talk about liquidity traps or that QE has not worked in Japan.

Bernanke says that QE is not inflationary, but that he is worried about deflation and won't let it happen....if QE is not inflationary then how can it fight deflation?

I don't believe QE is inflationary, its an asset swap (as Bernanke states). This doesn't mean that others won't believe it is inflationary and push up asset prices as a speculation.

I think the worst quote is when the interviewer asks whether he is able to control things and he said he was "100% confident". Famous last words.

He says the goal is to lower rates, yet doesn't talk about liquidity traps or that QE has not worked in Japan.

The Q Ratio and Other Measures Showing Market Overvaluation

As the markets have raced up this year (close to 20%) I have remained sanguine and continue to believe that the stock market is overvalued. What are the measures that I use to make this determination? The linked to blog above updates a few measures that have proved valuable in determining the long-term return of the markets (in the short-term is has zero predictability). The three measures are:

The relationship of the S&P Composite to a regression trendline

The cyclical P/E ratio using the trailing 10-year earnings as the divisor

The Q Ratio — the total price of the market divided by its replacement cost

All three measures show significant overvaluation in the S & P 500, the Q ratio showing the worst at 49%. The charts are below:

The relationship of the S&P Composite to a regression trendline

The cyclical P/E ratio using the trailing 10-year earnings as the divisor

The Q Ratio — the total price of the market divided by its replacement cost

All three measures show significant overvaluation in the S & P 500, the Q ratio showing the worst at 49%. The charts are below:

Subscribe to:

Posts (Atom)