Tuesday, May 24, 2011

The Meridian Has Moved

The Meridian Blog is still around, it just moved from Blogger to WordPress. It can be found Here.

Thursday, March 24, 2011

Movie Review: Inside Job

I finally was able to see the critically acclaimed documentary, Inside Job. The documentary was written, directed and produced by Charles Ferguson and recently won an Academy Award.

I had heard good reviews, but also heard that is was heavily slanted toward a view that Republicans were essentially the main cause of the crisis. I don't believe this too be accurate, the Democrats share just as much blame. In fact, the two parties worked very hard to be non-partisan in one area - Wall Street.

Inside Job does a great job of boiling down many of the root causes of the financial crisis (though not all of them). It was entertaining, educational and rightfully outrageous. Anger is the primary emotion I felt while watching. The one thing Inside Job does NOT leave you with is Hope. As I've stated many times over the past few years, Wall Street has become even more concentrated and powerful than ever, the exact opposite effect the crisis should have had.

We have a crisis in America, and it is only growing larger. That crisis is the control Wall Street has over our nation and its people. This is not a left wing or right wing observation, it's the reality. Until the banking industry is brought to heel, our nation will continue to be held hostage by Too Big Too Fail banksters.

Inside Job demonstrates the rise of the powerful financial industry and how deregulation fueled the fire. But it wasn't just Wall Street, Government failed the people and continues to do so. Both parties share responsibility, yet neither are willing to accept.

Few have been prosecuted, there is no Pecora Commission and financial reform was essentially defeated by the big banks.

I give Inside Job top ratings, its a great documentary that everyone should watch. You don't have to agree with Ferguson's politics to be outraged by what you will see.

While the movie offers little hope of change (how's that for irony), the fact that a movie like this was made at all and has gained so much fame is a positive sign.

Inside Job is available to rent now, I encourage you to watch.

Scott Dauenhauer, CFP, MSFP, AIF

Wednesday, March 23, 2011

Chart Store: Market Cap as a % of Nominal GDP

Prior to 1995 this measure of Stock Market Valuation had never been above 88% (this was right before the Crash of 1929). Since 1995 it has been over 100% the entire time with two brief movements below. The average is 62% - today it sits at about 125%, not an all time high (hit 180% in March of 2000), but still a number that should strike caution. Future returns from these levels do not look high.

Tuesday, March 22, 2011

Naked Capitalism: Regulatory Capture Is Alive & Well (

So yesterday I skewered Republicans for their lack of support of a Fiduciary Standard among all financial advice providers. Today I give equal time to their friends across the aisle, the Democrats.

Yves Smith over at Naked Capitalism Blog has a great article on Regulatory Capture:

Sleaze Watch: NY Fed Official Responsible for AIG Loans Joins AIG As AIG Pushes Sweetheart Repurchase to NY Fed

You can read the post, but the two doozies are:

Masaccio at FireDogLake was suitably outraged at this spectacle of a regulator getting a job with the biggest lobbying group in the industry he regulates…..and staying in his current oversight role:

The Washington Post reports that David H. Stevens will be taking over as head of the Mortgage Bankers Association. Stevens currently serves as Assistant Secretary for Housing in the Department of Housing and Urban Development, and as the Commissioner of the Federal Housing Administration. He has a conflict of interest so deep that he should be fired at once…

Allowing Stevens to stay on the job, and saying that it comports with ethics rules, is proof that the term “ethics” has lost all meaning. He is working on a settlement that in some news stories calls for a penalty of $20 billion, which only banksters think bears any relationship to the horrifying damage caused by these sharks, through jacked-up fees, fraudulent court filings, dual-track loan modifications and other sleazy tricks played on suffering homeowners. He comes from the industry, and is heading to the group that put out slimy reports condemning any steps that might aid homeowners, including judicial modification of mortgages in bankruptcy.

Why is he not immediately fired for cause? President Obama can’t even use his standard excuse, that we should look forward, not at the past. I’m looking forward, and I see a totally compromised person negotiating the future of millions of Americans.

So, a current official charged with heading the FHA (the main provider of all mortgages in the US right now) is leaving to head the Mortgage Bankers Association (an organization that has worked against consumers and modifications). This is a clear case of Regulatory Capture and a major ethics violation (or at least it should be).

As if that wasn't bad enough...more NY FED/AIG Corruption:

Aside from the hidden bailout, is that the NY Fed official who was responsible for overseeing Fed loans to TARP recipients, including the AIG loan, Brian Peters, joined AIG in late January. See this letter to the Committee on Oversight and Government Reform, based on subpoenaed information from the Fed, p. 8, the e-mail cited in footnote 31, for a sighting of Peters in action. Given the extensive interactions between the Fed and Treasury on the fight with Ken Lewis over his threat to walk from the Merrill purchase (the two were working in tandem here, and pretty much on all the major TARP recipients who got Fed loans), and the continued close cooperation between the Treasury and the NY Fed, it isn’t hard to imagine that Peters has good knowledge of and relationships with the key actors at the Treasury as well as at the NY Fed.

There is more to this Peters story, click the link to read it, but it is directly related to the current bid by AIG to buy assets from Maiden Lane II (owned by the Federal Reserve....The Taxpayers).

Obama promised change - so far all we've gotten is a further deepening of the financial services industry into government. This cannot end well. I guess I'd be more encouraged if there were an alternative, but the financial services industry owns the Republican party as well.

If this post seems to political - take out all references to Dem and Repubs and focus on the issue at hand - Regulatory Capture, the process where the industry being regulated hires those who have power over them and then uses those people to push their own agenda.

If you don't believe this is relevant I suggest you watch the documentary Inside Job, by Charles Ferguson.

Scott Dauenhauer CFP, MSFP, AIF

Does The Fed Even Understand Monetary Policy? Evidently Not

The United States is on a fiscal path towards insolvency and policymakers are at a "tipping point," a Federal Reserve official said on Tuesday.

"If we continue down on the path on which the fiscal authorities put us, we will become insolvent, the question is when," Dallas Federal Reserve Bank President Richard Fisher said in a question and answer session after delivering a speech at the University of Frankfurt.

Setting aside the massive budget deficits and whether or not fiscal austerity is a good/bad idea - its frightening that someone so powerful doesn't appear to understand our monetary system.

The United States is the sovereign monopoly issuer of its own non-convertible currency, it can not become "insolvent". The US has the ability to spend by crediting accounts (unlike states or european nations on the Euro) and thus is never fiscally restrained. This doesn't mean the US can spend at will with no consequences.

Is it possible Fisher does not know this?

Scott Dauenhauer CFP, MSFP, AIF

Monday, March 21, 2011

Hussman: Stock Not Always A Good Inflation Hedge

Hussman:

A paragraph from one of his recent missives:

This paragraph is saying two things - Stocks are valued quite high relative to the past and stocks don't always provide a hedge against inflation.

This is contrary to conventional wisdom.

Scott Dauenhauer CFP, MSFP, AIF

A paragraph from one of his recent missives:

Indeed, outside of the bubble period since the late 1990's, the only historical instance of Shiller P/Es materially above 24 was between August and early-October of 1929. The closest we got to 24 in post-war data was in mid-1965. While prices went on to achieve moderately higher levels (lagging earnings growth, so that the Shiller multiple fell), the mid-1965 valuation peak is widely viewed as the starting point for a 17-year "secular" bear market during which the S&P 500 achieved total returns of less than 5% annually through 1982, despite severe inflation. That's a good reminder that stocks are not a very good inflation hedge during periods when inflation is rising, particularly when stock valuations are already elevated and are priced to achieve poor returns. Stocks only "benefit" from inflation during hyperinflations and during sustained and anticipated inflations. In other cases, the eventual adjustments in economic activity and valuations overwhelm the "beneficial" effect of inflation on earnings.

This paragraph is saying two things - Stocks are valued quite high relative to the past and stocks don't always provide a hedge against inflation.

This is contrary to conventional wisdom.

Scott Dauenhauer CFP, MSFP, AIF

House Republicans to SEC: Halt fiduciary duty rulemaking - Investment News

House Republicans to SEC: Halt fiduciary duty rulemaking - Investment News

At least the Republican party is consistent. They have consistently sided with the financial services industry over the protection of consumers. During the Bush years when they had full control of Congress they catered to the whims of the financial and insurance industry and worked to allow conflicted advice to consumers. The Democrats haven't been much better in terms of catering to the financial services industry, but at least they are right on the issue of a universal fiduciary standard. House Republicans are not working to undermine the movement to ensure that ALL consumers have their interests put first.

I believe that all advisors should be held to the same standard, one that places the interests of their clients above their own (a fiduciary standard) - this doesn't actually sound controversial. Would you want your mother to work with someone who will work in her best interest or someone who is not required to work in her best interest? Evidently, the Republican party wants the latter. Very disappointing.

Scott Dauenhauer CFP. MSFP, AIF

At least the Republican party is consistent. They have consistently sided with the financial services industry over the protection of consumers. During the Bush years when they had full control of Congress they catered to the whims of the financial and insurance industry and worked to allow conflicted advice to consumers. The Democrats haven't been much better in terms of catering to the financial services industry, but at least they are right on the issue of a universal fiduciary standard. House Republicans are not working to undermine the movement to ensure that ALL consumers have their interests put first.

I believe that all advisors should be held to the same standard, one that places the interests of their clients above their own (a fiduciary standard) - this doesn't actually sound controversial. Would you want your mother to work with someone who will work in her best interest or someone who is not required to work in her best interest? Evidently, the Republican party wants the latter. Very disappointing.

Scott Dauenhauer CFP. MSFP, AIF

Friday, March 18, 2011

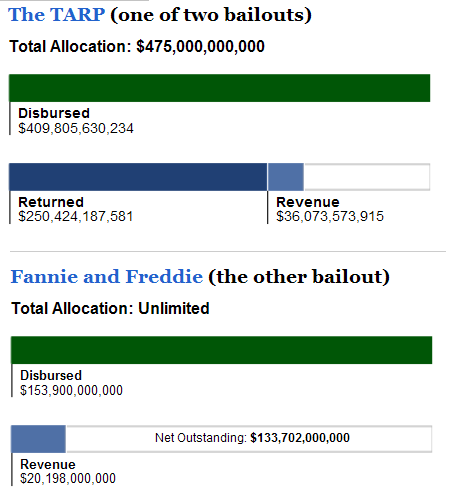

TARP is NOT Profitable

Barry Ritholz on his Big Picture Blog (www.ritzholz.com) has some great stuff on TARP and the GSE's and how far in the red the programs are. This is despite news reports that these programs are successful.

If you don't read his blog, its a good one.

Scott Dauenhauer CFP, MSFP, AIF

Sources:

Behind Administration Spin: Bailout Still $123 Billion in the Red

Paul Kiel

ProPublica, March 17, 2011, 10:27 a.m

http://www.propublica.org/article/behind-administration-spin-bailout-still-123-billion-in-the-red

The State of the Bailout

http://projects.propublica.org/bailout/main/summary

If you don't read his blog, its a good one.

Scott Dauenhauer CFP, MSFP, AIF

Sources:

Behind Administration Spin: Bailout Still $123 Billion in the Red

Paul Kiel

ProPublica, March 17, 2011, 10:27 a.m

http://www.propublica.org/article/behind-administration-spin-bailout-still-123-billion-in-the-red

The State of the Bailout

http://projects.propublica.org/bailout/main/summary

Fed Allows Increased Dividends - Continues War on Main Street

The Fed has decided to allow troubled banks to loot the taxpayers by allowing some to pay dividends and/or share buybacks.

This might sound like a boon and an encouraging sign of economic revitalization, but in reality it is a decision built upon a flawed capital model that ignores massive losses and potential losses sitting on the banks books.

Taxpayers are still on the hook for any bank failures in the future, not share or bondholders of these institutions. So while the banks pay out their large bonuses, big dividends and continue to burn cash that should be used to fix the problems they created, the nation remains mired in an economic drought with no end in sight.

Scott Dauenhauer, CFP, MSFP, AIF

Thursday, March 10, 2011

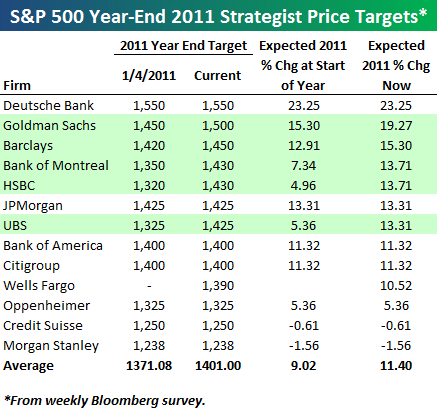

Strategist Price Targets for S &P 500 - Year End

Groupthink is alive and well on Wall Street:

GMO believes fair value to be around 900.

Scott Dauenhauer CFP, MSFP, AIF

GMO believes fair value to be around 900.

Scott Dauenhauer CFP, MSFP, AIF

Alt. Energy Update: Green Crude

OK, So these little Algae won't power the world, but they are more efficient than ethanol and switchgrass!

So far, the 30 or 40 mostly small companies now developing algae fuels in the U.S. have produced thousands of barrels of green crude, a far cry from the 7 billion barrels of oil consumed each year in America. Producers also face the daunting task of scaling from demonstration projects to what amounts to a vast new infrastructure for growing and maintaining algae in either fermentation tanks or in open ponds, and in providing feedstock for the plants, which grow best when fed sugars and other carbons in the form of plant waste or CO-2.

Green crude from algae is not a new idea. The federal government first started researching algae and other plants as alternative fuels at the National Renewable Energy Laboratory (NREL) in Golden, Colorado, after the first oil shocks in the 1970s. The program, however, was shut down in 1996 when oil dropped down below $40 a barrel.

Scott Dauenhauer CFP, MSFP, AIF

Monday, March 07, 2011

More MERS Trouble...Now in Oregon

Graphic Removed.

The linked to article above is a compilation of a few different articles, but explains in a very succinct fashion what MERS is and why this issue is so important - literally the solvency of our nations banking system is based on the legality of MERS.

I apologize if the above graphic doesn't fit within the window.

Scott Dauenhauer, CFP, MSFP, AIF

The linked to article above is a compilation of a few different articles, but explains in a very succinct fashion what MERS is and why this issue is so important - literally the solvency of our nations banking system is based on the legality of MERS.

I apologize if the above graphic doesn't fit within the window.

Scott Dauenhauer, CFP, MSFP, AIF

Monday, February 21, 2011

From Birinyi to Schiller to Gundlach - What Guru To Follow Makes a Difference

Robert Shiller sees a 13% total return for stocks.....for the decade, so the S & P ending around 1430.

Laszlo Birinyi sees the S & P at 2854 by.......2013.

Jeffrey Gundlach in Barrons this weekend says the S & P 500 is going to 500....this year.

So which is it? One guru (who has consistently been right, Shiller) see the S & P 500 at half what another sees it at, another sees the S & P 500 down 840 points THIS YEAR or next. Only one of these guys can be right (technically two as the market could go to 500 then 1430 or 2854....or vice versa).

What guru you follow makes a big difference in what returns you earn or how much money you lose. Predicting the future is not so simple, I'm throwing in more with Shiller, but admit anything can happen in this market (up or down).

Scott Dauenhauer CFP, MSFP, AIF

Laszlo Birinyi sees the S & P at 2854 by.......2013.

Jeffrey Gundlach in Barrons this weekend says the S & P 500 is going to 500....this year.

So which is it? One guru (who has consistently been right, Shiller) see the S & P 500 at half what another sees it at, another sees the S & P 500 down 840 points THIS YEAR or next. Only one of these guys can be right (technically two as the market could go to 500 then 1430 or 2854....or vice versa).

What guru you follow makes a big difference in what returns you earn or how much money you lose. Predicting the future is not so simple, I'm throwing in more with Shiller, but admit anything can happen in this market (up or down).

Scott Dauenhauer CFP, MSFP, AIF

Friday, February 18, 2011

Is the United States Just Like Greece? A Guru Gets It Wrong

Many years ago I read Fooled By Randomness, by Nassim Taleb - it was an instant classic in my library. I was excited when his next book Black Swan came out, it too was amazing. Both books seemed to predict in some way the financial crisis that eventually unfolded in 2008. If you haven't read either of these books it is my suggestion you pick them up and read and re-read them.

Needless to say, I'm a fan of Taleb. Yet Taleb has made some comments recently that can only be explained as mainstream and wrong - two things that he is rarely accused of.

At a forum in which he spoke recently he commented that "The United States is just like Greece, only without the International Monetary Fund (IMF) to enforce discipline". He goes on to say "The only happy thing that can happen in the U.S. is a bond riot".

Pretty much every mainstream economist, political commentator and politician (from left, right and center) has at some point expressed a similar refrain about the U.S. being Greece.

The reference is to the massive debt problem facing Greece and the dramatic events that led up to massive government (read Euro/IMF) intervention last year.

With the United States National Debt approaching $14 trillion, the comparison would seem to make sense on some level - but the fact is that it is wrong. The U.S. is not Greece and is not like Greece.

The big flaw in Taleb's arguement is a misunderstanding of the monetary system under which each country operates. Greece is a member of the European Union and borrows in Euro's, a currency in which it has no control and little influence. Greece must acquire Euro's by selling something in order to pay their debts, they can't print the Euro. The United States on the other hand issues debt in their own non-convertible currency, they are the monopoly issuer and can print dollars. The U.S. cannot default (ok, they could, but it would be a political decision, not a revenue constraint) as they owe dollars of which they control the printing press.

A more apt, but still not a good comparison would be California and Greece. California spends and borrows in dollars, the state must receive tax revenue or issue debt in dollars. California cannot print dollars, thus they are revenue constrained and could default (note: States cannot currently go bankrupt, nor do I believe that any states will....at this point).

The common belief is that the Federal Reserve is "printing money" via their Quantitative Easing programs, this is not true - they are changing the duration of government liabilities - essentially engaging in Open Market Operations. It is the Federal Government (Both Houses of Congress and the Presidency) that actually print money (out of thin air) when they deficit spend.

When one of the greatest thinkers in the financial markets doesn't understand the global monetary systems, it makes one wonder what hope there is for our financial systems.

Please note I am not saying Taleb is not smart, I think he is a genius, but he has this wrong - as do most mainstream economists.

Scott Dauenhauer CFP, MSFP, AIF

Tuesday, February 15, 2011

Is MERS dying? NY Judge declares MERS Biz model "Not supported by law"

Why this story is not frontpage news I'll never know, but this ruling could be another nail in the coffin for the Mortgage recordkeeping system known as MERS. Given what is at stake there are a lot of panicked executives in MERS land and they likely work for the Too Big Too Fail banks.

The market had zero reaction because it knows that the financial system is allowed to carry worthless mortgages at next to 100% of value on their balance sheets, so no real risk to capital exists (this is there thinking).

Another step in the MERS journey is complete, what will be next?

Scott Dauenhauer CFP, MSFP, AIF

Wednesday, February 09, 2011

Monday, February 07, 2011

Lack of Imagination or Too Much Imagination?

The continued full steam ahead bull market in stocks has caught many (including myself) by surprise. Its not that I didn't believe this meteoric rise couldn't happen, just that I thought perhaps the market had learned something from a decade of multiple 50% crashes and bubbles.

At these market levels stocks are priced for perfection and any hiccup could present a large downside. Currently, the market pendulum has swung to an "Imagination" of future, ongoing prosperity for all and has forgotten what happen just a few short year ago. But is this a good thing? For those who invest in stocks I think you must have a different "Imagination" - what can go wrong and what are the downside consequences.

There are so many things that can go wrong and there is no or little Margin of Safety left in the market. Just a few things:

Terrorist attack

Pandemic

Superstorms

Oil disruption

Internet attack that cripples communications as we currently know them

American Austerity

Steve Jobs take another leave of absence (wait, that happened! Please come back Steve, get better).

My point is not that you shouldn't invest when bad things can happen - bad things can and DO always happen (too use a way overused term - Black Swans). The threat of bad and unexpected events shouldn't keep one from investing in stocks, however when you do decide to invest there needs to be a margin built into your purchase that accounts for the possibility of bad things happening (an expectation if you will). That way, you know you still have value in your purchase when/if things do go bad and you won't have to panic sell (thus feeding the beast).

For example, when Reagan took office unemployment was sky high, inflation was rampant, the economy was just in big trouble. Yet stocks were trading at only 8 times prior cyclically-adjusted earning. The market suffered from a lack of "Imagination" as to what could go right. But those people who invested in stocks had a huge margin of safety - things didn't have to go very right for them to receive a reasonable return on stocks. This is not the case today - in an economy that is much more difficult than 1980/81 we have stocks bid up to levels that were only seen prior to major stock market tops. The stock market suffers from a lack of imagination of what could go wrong and has priced in perfection and almost zero Margin of Safety.

History has taught us that these exuberant times can continue and for much longer than any of us ever imagine (NASDAQ, Housing, etc).

There is little margin for error, very little imagination and we should be cautious at this juncture.

Scott Dauenhauer CFP, MSFP, AIF

At these market levels stocks are priced for perfection and any hiccup could present a large downside. Currently, the market pendulum has swung to an "Imagination" of future, ongoing prosperity for all and has forgotten what happen just a few short year ago. But is this a good thing? For those who invest in stocks I think you must have a different "Imagination" - what can go wrong and what are the downside consequences.

There are so many things that can go wrong and there is no or little Margin of Safety left in the market. Just a few things:

Terrorist attack

Pandemic

Superstorms

Oil disruption

Internet attack that cripples communications as we currently know them

American Austerity

Steve Jobs take another leave of absence (wait, that happened! Please come back Steve, get better).

My point is not that you shouldn't invest when bad things can happen - bad things can and DO always happen (too use a way overused term - Black Swans). The threat of bad and unexpected events shouldn't keep one from investing in stocks, however when you do decide to invest there needs to be a margin built into your purchase that accounts for the possibility of bad things happening (an expectation if you will). That way, you know you still have value in your purchase when/if things do go bad and you won't have to panic sell (thus feeding the beast).

For example, when Reagan took office unemployment was sky high, inflation was rampant, the economy was just in big trouble. Yet stocks were trading at only 8 times prior cyclically-adjusted earning. The market suffered from a lack of "Imagination" as to what could go right. But those people who invested in stocks had a huge margin of safety - things didn't have to go very right for them to receive a reasonable return on stocks. This is not the case today - in an economy that is much more difficult than 1980/81 we have stocks bid up to levels that were only seen prior to major stock market tops. The stock market suffers from a lack of imagination of what could go wrong and has priced in perfection and almost zero Margin of Safety.

History has taught us that these exuberant times can continue and for much longer than any of us ever imagine (NASDAQ, Housing, etc).

There is little margin for error, very little imagination and we should be cautious at this juncture.

Scott Dauenhauer CFP, MSFP, AIF

Thursday, February 03, 2011

Tuesday, January 25, 2011

Hussman: "We've laid a lovely turf over a toxic waste dump"

In John Hussman's latest commentary he explains the constraints of Monetary Policy, but he also takes a shot at how the United States has handled our financial crisis:

As for the U.S. financial system - particularly major banks - I am continually perplexed by the juxtaposition of tens of millions of underwater mortgages and millions of delinquent and unforeclosed homes, coupled with a set of FASB accounting rules (revised at the height of the recent crisis) that allows these debts to be carried at face value upon the discretion of the banks that report the data. I'll say one thing - it should take less than two seconds of thought to recognize that allowing dividends, bonuses, and other withdrawals of capital - without the requirement that banks mark their assets to market - is quite literally how Ponzi schemes function. We've laid a lovely turf lawn over a toxic waste dump, and are all too willing to assume that the underlying issues have been solved. The FASB and the Fed have turned the U.S. banking system into the Love Canal.

John's observation that we shouldn't allow banks to pass out money to shareholders and management while an enormous amount of toxic assets remain on the balance sheet is important, we will soon see how far regulatory capture has gone.

Scott Dauenhauer CFP, MSFP, AIF

Friday, January 21, 2011

Mass Supreme Court to Consider Whether Buyers Out of Faulty Foreclosures Actually Own Property

Mass Supreme Court to Consider Whether Buyers Out of Faulty Foreclosures Actually Own Property

So you bought a home in foreclosure, you own it - right? Not so fast. The Mass Supreme court may make things very uncomfortable for the banks. This is a case that everyone who owns bank stocks (or any stocks) should be following closely.

Scott Dauenhauer

So you bought a home in foreclosure, you own it - right? Not so fast. The Mass Supreme court may make things very uncomfortable for the banks. This is a case that everyone who owns bank stocks (or any stocks) should be following closely.

Scott Dauenhauer

Wednesday, January 19, 2011

PragCap: Putting the Muni Bond Panic Into Perspective

Cullen Roche has a well timed, short blog post on the latest Meredith Whitney "call" on the muni markets - the smart money isn't buying it.

The entire piece can be read in three minutes and is worth a read if you own muni's or are looking to.

Scott

First of all, if the USA is willing to save banks and let states fail then the purpose of this country has failed and we should just fold up shop and thank everyone for being a citizen for all these years. Second, we have the mechanism in place to avoid a Euro style crisis. Unlike the Europeans, who lack the proper tools to deal with their own crisis, the USA is fully united and established a central treasury long ago. The funding mechanism for crises is ready to roll should it ever be needed. If ever there was a need for a “Geithner Put” I have little doubt that this administration would utilize it. After all, no one fails in this “capitalist” world anymore. Third, we’re far more likely to see increased austerity measures (such as the tax increases in Illinois) as opposed to defaults. The credit crisis is still causing ripples across the world, but one thing it is not doing is turning the USA into Europe.

The entire piece can be read in three minutes and is worth a read if you own muni's or are looking to.

Scott

Friday, January 14, 2011

Wednesday, January 12, 2011

Goldman Sachs: S & P 500 Will be up 18% in 2011 - Should You Trust Them?

Can you trust Goldman Sachs? The answer has to be no. But can they forecast? Well, David Kostin is out with his latest forecast and says the S & P 500 will rally 18% in 2011. It very well may, or it may not - but how has Goldman done in the recent past and did they predict the stock market crash (I'm not saying I did, I don't make short term predictions)? Well, below is from wikipedia, it is a short synopsis of their old Chief Prognosticator Abby Joseph Cohen:

I wouldn't put much "stock" in Goldman forecasts (unless of course they are building a financial product they want to short).

Scott Dauenhauer CFP, MSFP

A Little Goldman History - Abby Joseph Cohen

She is famous for predicting the bull market of the 1990s early in the decade. However, she failed to predict the dramatic stock market decline of the early 2000s and developed a reputation as a so-called "perma-bull" and was ridiculed for her continuous bullish predictions after March 2000 as market indices fell. Her reputation was further damaged when she failed to foresee the great crash of 2008.

On a CNBC appearance in March 2008, she predicted S&P 500 at 1550 by end 2008.

In an August 10, 2007 appearance on CNBC Abby Joseph Cohen predicted the S&P 500 would rally to 1,600 by December.

In December 2007 Abby Joseph Cohen predicted the S&P 500 index would reach 1,675 in 2008. The S&P 500 traded as low as 741.02 by November 2008.

On March 8, 2008 Goldman Sachs announced that Abby Joseph Cohen was being replaced by David Kostin as the bank's chief forecaster.

I wouldn't put much "stock" in Goldman forecasts (unless of course they are building a financial product they want to short).

Scott Dauenhauer CFP, MSFP

Monday, January 10, 2011

Sunday, January 09, 2011

Oregon Ducks Power Ballad - Go Duck

I'm a huge Oregon Ducks fan, tomorrow they play in the BCS! GO DUCKS!!!

Thursday, January 06, 2011

Gallup Finds Unemployment at 9.6% in December

Unemployment should be falling, in fact at this point in time in a "recovery" we should be seeing steady net job creation. Instead the most broad measure of unemployment continues to rise.

Gallup Finds Unemployment at 9.6% in December

Wednesday, January 05, 2011

Schiller: S & P 500 will be up 13%...between now and 2020

Famed economist Robert Schiller who was one of the first to call the stock market and real estate bubbles believes that the stock market in general will rise by a total of 13% over the next decade. An extremely bearish forecast, but based on very real analysis of historic valuations. Schiller is not making this determination based upon any view of the current economy, it is a simple historic extrapolation of stock market mean reversion.

Subscribe to:

Posts (Atom)